Most businesses have a carbon footprint they can see: the fuel in their fleet, the gas powering their boilers, the electricity bill arriving each month. They also have a much larger footprint they cannot see easily i.e. the emissions embedded in everything they buy, ship, and sell.

Scope 1, 2, and 3 emissions is the framework that makes both visible.

For sustainability professionals building a carbon accounting programme, and for business leaders navigating regulatory requirements under CSRD, GHG Protocol, or SBTi, understanding the three scopes is not optional groundwork. It is the foundation on which every credible emissions reduction strategy is built.

This guide covers how the greenhouse gas protocol classifies each scope, how to calculate your emissions, what the regulations require, and where the biggest opportunities to lower emissions sit across your value chain.

Keep reading.

What are scope 1, 2, and 3 emissions?

Scope 1, 2, and 3 emissions are a classification system for a company’s greenhouse gas emissions, organized by source and by the level of control the company has over them. The framework was developed by the GHG Protocol, a joint initiative of the World Resources Institute (WRI) and the World Business Council for Sustainable Development (WBCSD). The GHG Protocol Corporate Accounting and Reporting Standard was first published in 2001 and has since become the global benchmark for corporate carbon accounting.

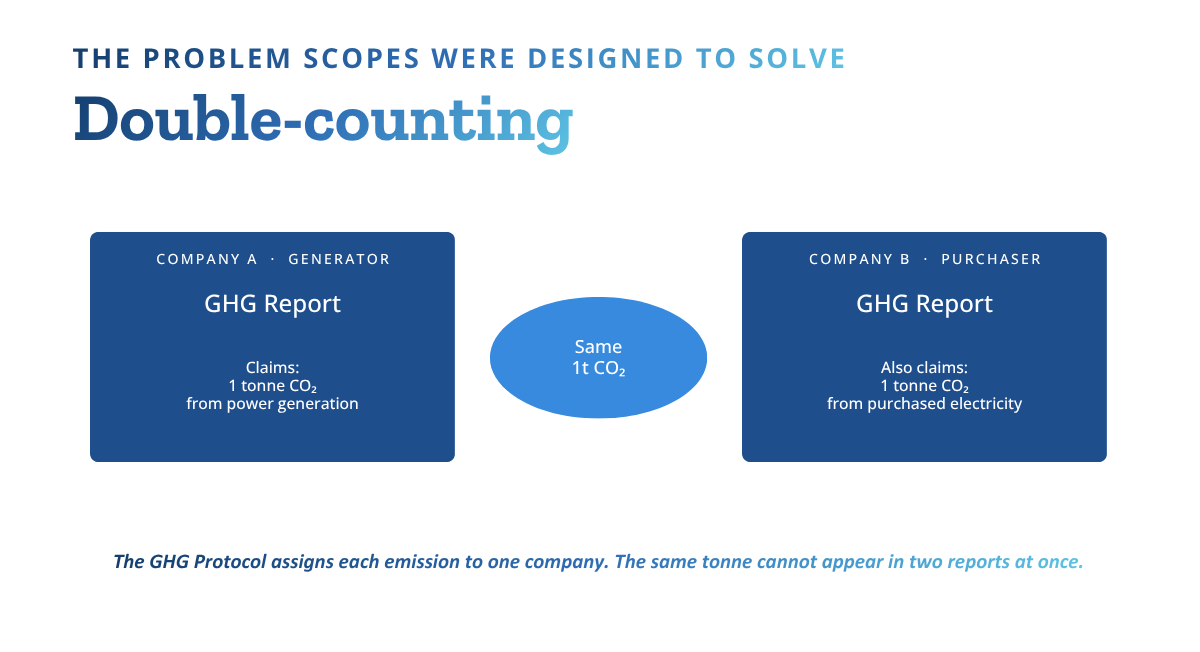

The three scopes exist to solve a specific accounting problem: Double-counting.

Without a consistent classification system, the same tonne of CO₂ could legitimately appear in multiple companies’ reports simultaneously.

A power station’s output, for example, could be claimed by both the generator and every business that purchased electricity from the grid.

The scope system assigns each emission to the company best placed to control or influence it, creating a coherent picture of the company’s greenhouse gas emissions without overlap.

The result is three distinct categories:

Scope 1 emissions are direct GHG emissions from sources owned or controlled by your company.

Scope 2 emissions are indirect GHG emissions from the generation of purchased electricity, heat, steam, or cooling consumed by your company.

Scope 3 emissions are all other indirect emissions that occur in your company’s value chain, both upstream and downstream, and are not already captured in Scope 2.

Together, the three emissions scopes give a complete picture of a company’s total emissions: what it burns, what it buys for energy, and what it causes across its supply chain and product lifecycle.

Scope 1 emissions: Direct emissions

Scope 1 emissions are the direct GHG emissions produced from sources your company owns or controls. Any greenhouse gas released as a direct result of your company’s own operations falls here, whether from burning fuel, running production processes, operating company vehicles, or unintended releases from equipment.

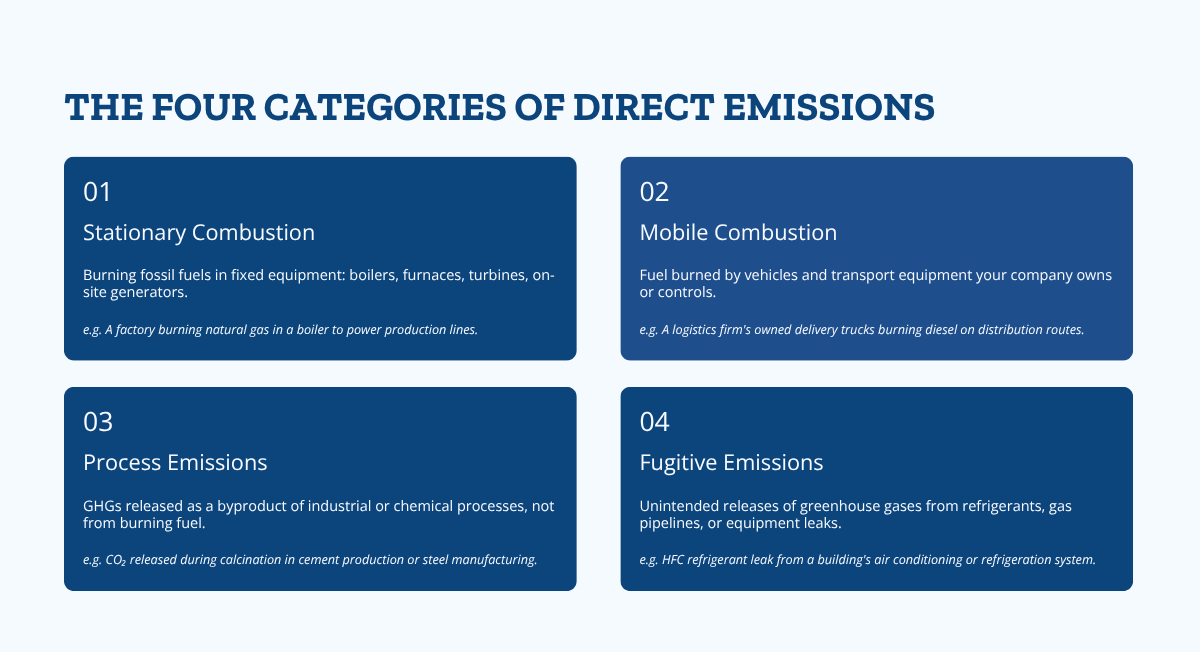

The GHG Protocol organizes direct emissions into four sub-categories:

Stationary combustion: Emissions from burning fossil fuels in fixed equipment such as boilers, furnaces, turbines, and on-site generators. A manufacturing plant running gas-fired boilers is generating stationary combustion emissions every hour of production.

Mobile combustion: Emissions from fuel burned by vehicles owned or operated by your company. This includes company cars, delivery trucks, forklifts, ships, and aircraft that appear on your company’s balance sheet or are under your operational control.

Process emissions: GHGs released as a byproduct of industrial processes rather than energy use. Chemical reactions in cement production, steel manufacturing, and fluorochemical processing generate direct GHG emissions that are distinct from any fuel combustion involved.

Fugitive emissions: Unintended releases of greenhouse gases, typically refrigerants leaking from air conditioning or refrigeration systems, or equipment leaks from gas pipelines and compressors. These are easy to overlook in an emissions inventory but can carry significant global warming potential, particularly where HFCs are involved.

Industry examples across sectors:

A car manufacturer’s Scope 1 emissions include the natural gas burned in paint booths and assembly processes, diesel consumed by site vehicles, and refrigerant losses from facility air conditioning. A logistics company’s Scope 1 is dominated by diesel across vehicles owned and operated for deliveries. A hotel group’s Scope 1 covers fuel combustion in on-site boilers, gas-fired kitchen equipment, and fugitive emissions from large cooling systems.

Calculating Scope 1 emissions follows the standard GHG Protocol methodology: activity data multiplied by an emission factor.

You measure the quantity of fuel burned, refrigerant lost, or material processed, then apply the appropriate emission factor from a recognized database such as the UK DEFRA emission factors, the US Environmental Protection Agency’s emissions factors hub, or IPCC defaults. The output is expressed in tonnes of CO₂ equivalent (tCO₂e).

Scope 1 is generally the most straightforward scope to measure. Your company is solely responsible for these emissions sources, and the underlying data sits entirely within your own operations. The main challenge is ensuring all sources are captured, particularly fugitive emissions, which require systematic leak detection rather than billing records.

Scope 2 emissions: Indirect energy emissions

Scope 2 emissions are the indirect GHG emissions associated with purchased electricity, heat, steam, or cooling consumed by your company. The physical emissions occur at the power station or energy facility, not at your site. Because your energy demand drives their generation, however, the GHG Protocol attributes them to your company’s carbon footprint.

For most office-based and service sector businesses, Scope 2 represents the largest controllable share of their direct carbon footprint. For energy-intensive industries, it can be substantial even alongside significant Scope 1 figures.

Location-based vs market-based accounting

The GHG Protocol’s Scope 2 Guidance introduced two separate accounting methods, and understanding the difference matters considerably for reporting accuracy.

The location-based method calculates emissions using the average carbon intensity of the electricity grid in the country or region where your facility operates. If your grid is predominantly coal or gas-fired, your location-based Scope 2 figure reflects that reality, regardless of what energy products you have contracted.

The market-based method reflects the specific electricity products your company has contracted or purchased. If your company holds renewable energy certificates (RECs in the US, Guarantees of Origin in Europe), those certificates allow you to report lower or zero Scope 2 emissions under the market-based method, provided the certificates are valid, retired, and matched to your actual consumption.

Both figures are required under CSRD reporting. The gap between them is often where scrutiny from auditors and investors lands. A company reporting zero market-based Scope 2 while showing high location-based emissions raises questions about the quality of its renewable energy procurement.

Note: the GHG Protocol’s Scope 2 Guidance is currently under revision. The formal public consultation opened in late 2025, with revised drafts circulating through 2026 and final publication anticipated toward the end of 2027. The updated guidance is expected to tighten the conditions for market-based reporting, including requirements for hourly and geographic matching between renewable energy certificates and actual consumption.

One important clarification: Hourly matching is not required when using residual mix emission factors. Companies relying on RECs or Guarantees of Origin for market-based Scope 2 reporting should review their certificate procurement approach ahead of the final publication.

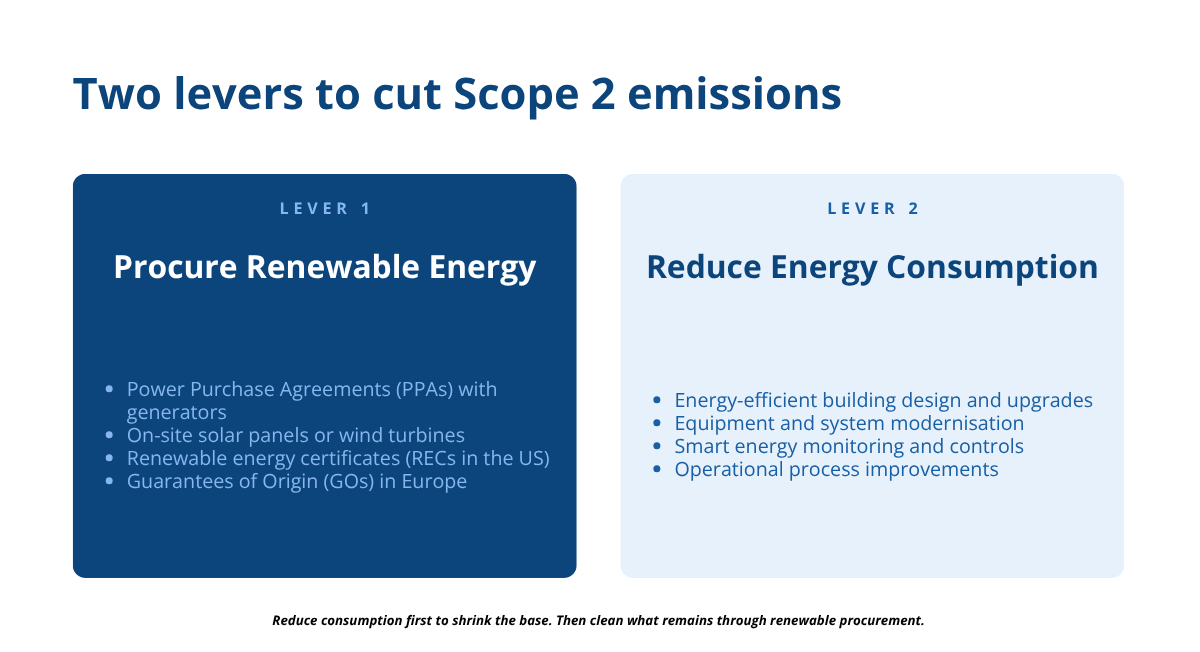

Reducing Scope 2 emissions comes down to two primary levers. The first is procuring renewable electricity through power purchase agreements (PPAs) with generators, on-site solar or wind turbines, or credible certificate schemes.

The second is reducing total purchased energy consumption through energy efficient building design, equipment upgrades, and operational improvements, cutting the emissions base before procurement strategies are applied.

Scope 3 emissions: Value chain emissions

Scope 3 emissions are all other indirect emissions that occur in a company’s value chain. These are the emissions your company is indirectly responsible for: Emissions caused by your purchasing decisions upstream, and emissions generated by the use and disposal of your products downstream.

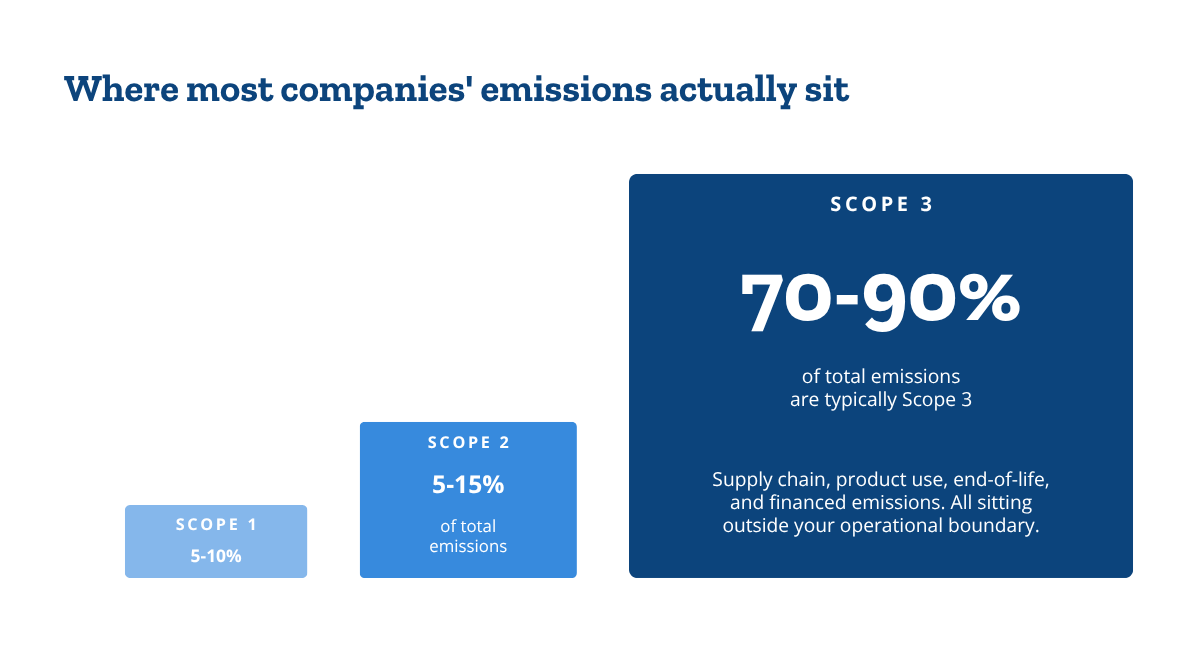

For most companies, Scope 3 emissions represent between 70 and 90 percent of their total carbon footprint. A car manufacturer’s factory emissions are a fraction of the lifetime driving emissions from every vehicle it sells. A financial institution’s own operations are negligible compared to the financed emissions across its loan and investment portfolio. A retailer’s direct GHG emissions from stores and offices are dwarfed by the embedded carbon in the goods it sources and the transport in its supply chain.

This concentration of emissions in Scope 3 is not just a reporting fact. It is a strategic one. The biggest lever for most companies’ total emissions lies outside their own operations, in the supply chain and in the hands of their customers.

The 15 categories of Scope 3 emissions

The GHG Protocol organizes all value chain emissions into 15 categories, split between upstream and downstream:

Upstream Scope 3 (categories 1-8) covers emissions from purchased inputs and activities before they reach your operations:

| Category | Description |

|---|---|

| 1. Purchased goods and services | Emissions from producing everything your company buys |

| 2. Capital goods | Emissions from producing long-term assets your company acquires |

| 3. Fuel and energy-related activities | Extraction and production of fuels and energy not in Scope 1 or 2 |

| 4. Upstream transportation and distribution | Freight and logistics in your supply chain |

| 5. Waste generated in operations | Disposal and treatment of waste your operations produce |

| 6. Business travel | Flights, rail, and accommodation for employees |

| 7. Employee commuting | Emissions from staff travelling to and from work |

| 8. Upstream leased assets | Emissions from assets you lease from others |

For companies importing goods into the EU, CBAM adds a direct compliance dimension to Scope 3 Category 1.

Use the CBAM Supplier Data Checklist to make sure your supplier carbon data meets the requirement.

Downstream Scope 3 (categories 9-15) covers emissions from your products and activities after they leave your operations:

| Category | Description |

|---|---|

| 9. Downstream transportation and distribution | Freight from your facilities to customers |

| 10. Processing of sold products | Further manufacturing of intermediate products by customers |

| 11. Use of sold products | Emissions generated when customers use what you sell |

| 12. End-of-life treatment of sold products | Waste disposal of products after customer use |

| 13. Downstream leased assets | Emissions from assets you lease to others |

| 14. Franchises | Emissions from franchisee operations |

| 15. Investments | Financed emissions from financial institutions |

Why Scope 3 is hard to measure

The challenge with Scope 3 is data. Unlike Scope 1 and 2, where your own operational records are the source, Scope 3 depends on supplier data, third-party logistics records, customer behaviour data, and product lifecycle information that is often incomplete, inconsistent, or estimated using spend-based proxies.

Working through your Scope 3 supplier data?

Identifying emission hotspots across a supply chain with hundreds or thousands of suppliers requires systematic data collection that most companies are still building. Category 1 (purchased goods and services) alone can span the entire procurement process, from raw materials through to finished goods, each with its own embedded carbon.

This data challenge is why carbon accounting software built for Scope 3 data collection earns its place in a serious carbon accounting programme. Automating supplier data requests, applying current emission factors, and flagging data gaps reduces the manual effort significantly and produces results that can withstand external verification.

Scope 1 vs 2 vs 3: Key differences

| Scope 1 | Scope 2 | Scope 3 | |

|---|---|---|---|

| Type | Direct emissions | Indirect (purchased energy) | Indirect (value chain) |

| Source | Owned or controlled sources | Purchased electricity, heat, steam, cooling | All other upstream and downstream activities |

| Company control | High | Medium | Low |

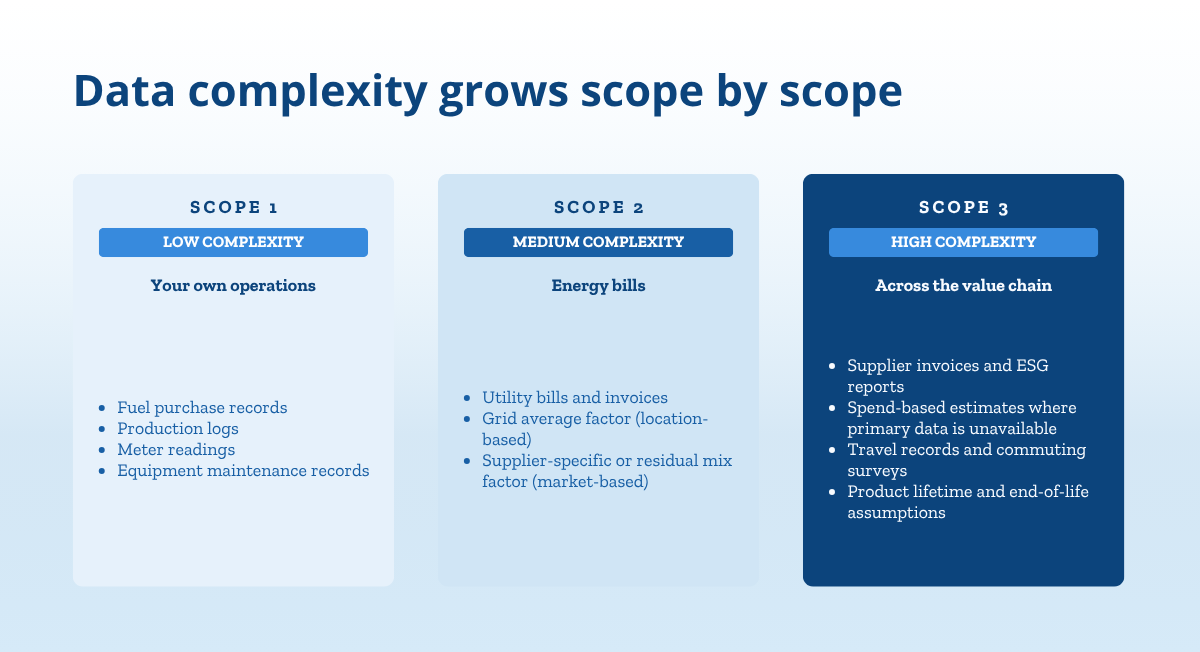

| Data difficulty | Low | Low to medium | High |

| Typical footprint share | 5-10% | 5-15% | 70-90% |

| Key reduction lever | Fuel switching, electrification | Renewable energy procurement, PPAs | Supplier engagement, product design |

| Regulatory requirement | Mandatory (CSRD, GHG Protocol) | Mandatory (CSRD, GHG Protocol) | Mandatory for material categories (CSRD); required for SBTi net zero |

Which scopes must your company report?

Regulatory requirements for scope emissions vary by framework. The answer to “which scopes are mandatory” depends on which regulation or standard applies to your business.

CSRD (Corporate Sustainability Reporting Directive): Under the European Sustainability Reporting Standards (ESRS E1), Scope 1 and Scope 2 emissions are mandatory for all in-scope companies. Scope 3 reporting is required for all categories identified as material through a double materiality assessment. In practice, most large companies with any meaningful supply chain or product footprint will find multiple Scope 3 categories to be material, making Scope 3 reporting effectively mandatory under CSRD.

GHG Protocol Corporate Standard: Scope 1 and Scope 2 are required. Scope 3 is strongly encouraged but not mandated under the base Corporate Standard. Companies that separately apply the GHG Protocol Scope 3 Standard are required to report all relevant categories identified as material.

SBTi (Science Based Targets initiative): Companies setting net zero targets under the SBTi Corporate Net-Zero Standard must set reduction targets covering all three scopes. Scope 3 targets are a non-negotiable element of net zero validation under SBTi methodology.

IFRS S2 (ISSB): Requires disclosure of Scope 1, Scope 2, and significant Scope 3 emissions. As more jurisdictions adopt or reference IFRS S2, full scope coverage is becoming a baseline expectation for listed companies globally.

How to calculate your scope emissions

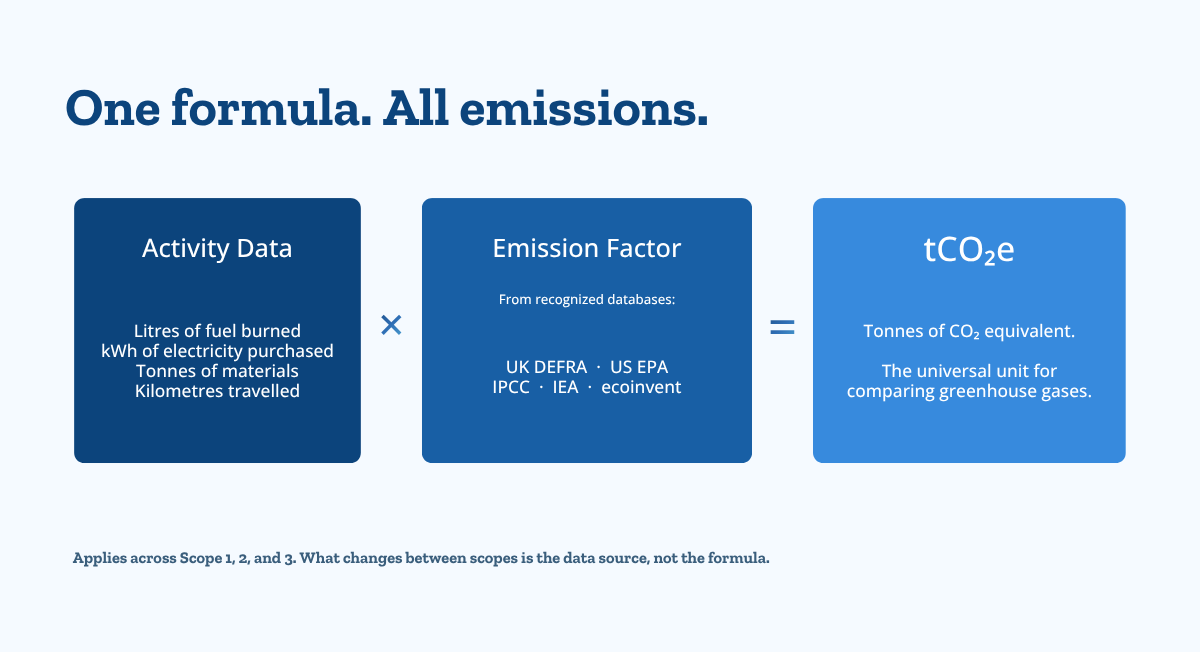

The calculation methodology for all three scopes follows the same core formula:

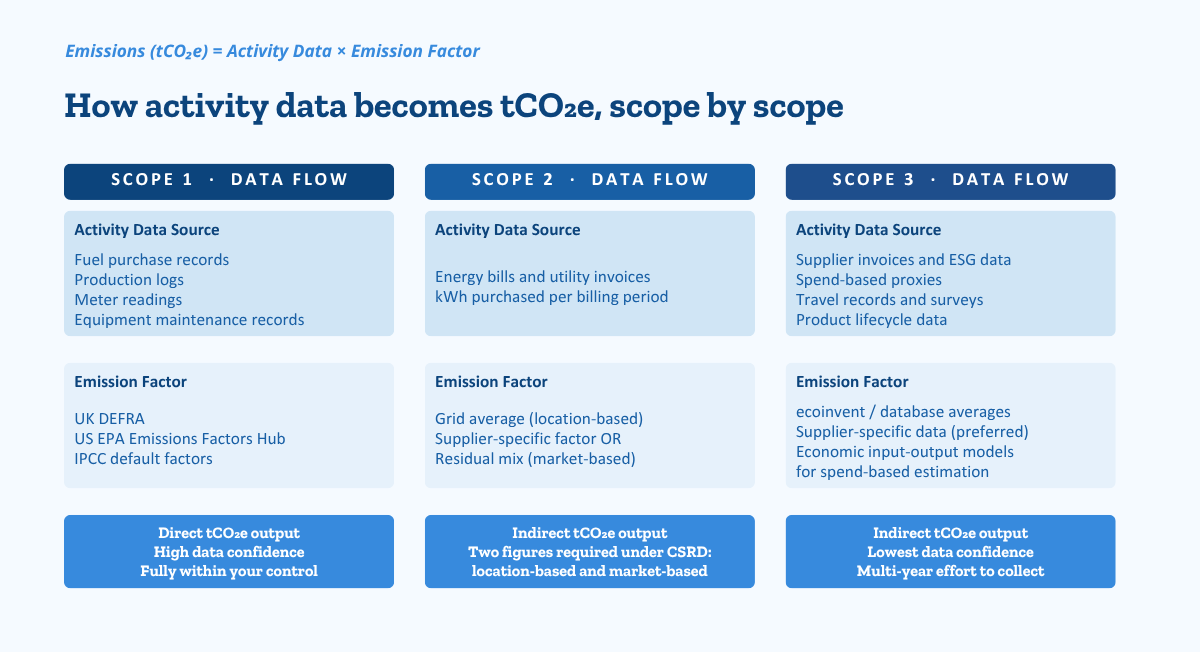

Emissions (tCO₂e) = Activity data × Emission factor

Activity data is a measured quantity: litres of diesel consumed, kWh of electricity purchased, tonnes of raw materials procured, kilometres travelled for business purposes. The emission factor converts that activity into a CO₂ equivalent figure, drawing on recognized databases including UK DEFRA, the EPA’s emission factors hub, the IEA electricity emission factors, or product-level databases such as ecoinvent for supply chain calculations.

The methodology in practice varies by scope.

For Scope 1, activity data comes directly from your own operations: Fuel purchase records, production logs, meter readings, and equipment maintenance records for fugitive emissions. Measurement here is primarily an internal data management challenge.

For Scope 2, your energy bills provide the core activity data. Applying the right emission factor requires knowing which method you are using: a grid average factor for location-based, or a supplier-specific or residual mix factor for market-based reporting.

For Scope 3, data collection is considerably more complex. Category 1 (purchased goods and services) may require spend-based estimation using economic input-output models where supplier-specific data is unavailable. Categories like business travel and employee commuting can draw on travel booking records and commuting surveys. Categories like use of sold products and end-of-life treatment require assumptions about customer behaviour and product lifetime.

Building a complete Scope 3 inventory is a multi-year process for most companies. The GHG Protocol recommends starting with a screening exercise to identify emission hotspots before committing to full primary data collection across all 15 categories.

How to reduce emissions across all three scopes

Measuring scope 1 2 3 emissions is a means to an end. The strategic value is in the reduction.

Scope 1: The primary levers are fuel switching and electrification. Replacing gas-fired boilers with heat pumps, transitioning company vehicles to electric vehicles, and redesigning production processes to reduce fossil fuel dependency all cut direct GHG emissions at the source. For process emissions generated through chemical reactions or industrial activity, reduction requires process redesign, raw materials substitution, or investment in carbon capture. The path is clear; the timeline depends on capital availability and technology readiness.

Scope 2: The fastest route to lower Scope 2 emissions is procuring renewable electricity through power purchase agreements or on-site generation from solar panels or wind turbines. Reducing total energy use through energy efficient equipment, insulation upgrades, and operational practices reduces the purchased energy base before procurement strategies are applied. For CSRD reporters, renewable procurement needs to meet the market-based criteria under the updated Scope 2 Guidance, not just certificate purchases that are geographically or temporally mismatched.

Scope 3: This is where comprehensive strategies require the most sustained effort. For upstream supply chain emissions, the primary levers are supplier engagement, low-carbon procurement criteria embedded into the procurement process, and collaborative programmes with key suppliers to reduce their own Scope 1 and 2 emissions. For downstream emissions, product design is the main tool: extending product lifetime, enabling repair and reuse, reducing the carbon intensity of the use phase, and designing for lower-impact end-of-life treatment.

Companies that track carbon emissions across all three scopes using a platform aligned to GHG Protocol methodology can identify where their reduction efforts will have the greatest impact per pound or euro of investment, and report progress credibly to regulators, investors, and customers.

Here’s how to chalk out a decent decarbonisation strategy for your organisation.

So, to recall….

Scope 1, 2, and 3 emissions give companies a complete map of their carbon footprint. Scope 1 covers what you burn. Scope 2 covers what you buy for energy. Scope 3 covers everything else across your value chain.

Together, they are the basis for credible net zero strategy, regulatory compliance under CSRD and ISSB, and science-based target setting with SBTi. Reporting only Scope 1 and 2 while ignoring Scope 3 leaves the largest share of most companies’ emissions entirely unaccounted for.

Getting all three right is not a sustainability exercise. It is a risk management one.

The Credibl platform automates Scope 1, 2, and 3 data collection, applies current emission factors, and generates audit-ready reports aligned to CSRD, GHG Protocol, and SBTi requirements.

Frequently asked questions

What is the difference between Scope 1, 2, and 3 emissions?

Scope 1 emissions are direct GHG emissions from sources your company owns or controls, such as fuel combustion and company vehicles. Scope 2 emissions are indirect emissions from purchased electricity or energy. Scope 3 emissions are all other indirect emissions across your value chain, including supply chain emissions upstream and product use emissions downstream.

Why does the GHG Protocol use three scopes?

The three-scope system prevents double-counting. By assigning each emission to the company most responsible for controlling or influencing it, the GHG Protocol ensures the same tonne of CO₂ does not appear in multiple companies’ inventories at the same time.

Is Scope 3 reporting mandatory?

Under CSRD, Scope 3 reporting is required for all categories identified as material through a double materiality assessment. Under the SBTi Corporate Net-Zero Standard, Scope 3 targets are required for validation. Under the base GHG Protocol Corporate Standard, Scope 3 is encouraged but not mandated.

What percentage of a company’s emissions are typically Scope 3?

or most companies, Scope 3 emissions represent between 70 and 90 percent of total emissions. In sectors with complex supply chains or high-use-phase carbon intensity, such as automotive, consumer electronics, or financial services, the proportion can be higher.

What is the difference between location-based and market-based Scope 2 accounting?

Location-based Scope 2 uses the average carbon intensity of the electricity grid in the region where your facility operates. Market-based Scope 2 reflects the specific energy products your company has contracted, including renewable energy certificates. CSRD requires disclosure of both figures.

How do you start measuring Scope 3 emissions?

Begin with a screening exercise across all 15 GHG Protocol categories to identify which are relevant and material for your business. Prioritize the highest-emission categories, use spend-based estimates where supplier data is not yet available, and build toward primary data collection from key suppliers over time. A carbon accounting platform can automate much of this process and flag data gaps for remediation.