Most organisations know they need a materiality assessment. Fewer know how to run one that actually holds up – under audit, under board scrutiny, and under the increasingly sharp eye of CSRD regulators.

KPMG’s 2025 Survey of Sustainability Reporting concluded nearly half of the world’s largest companies now conduct a double materiality assessment, driven largely by CSRD requirements.

This guide is for the sustainability lead or ESG consultant who is past the “what even is this?” stage and firmly into “how do we do this properly?” territory. We cover the full process, from stakeholder mapping to materiality matrix, and what happens after the matrix — which is where most teams quietly lose the thread.

Want to skip straight to the doing? Take this with you.

Credibl’s ESRS-aligned Double Materiality Assessment Template, built on the EFRAG IG 1 methodology, with scoring formulas, stakeholder input columns, and a Not Material justification section included.

What Is an ESG Materiality Assessment (And Why Is It a Key Tool for Corporate Sustainability)?

An ESG materiality assessment is a structured process for identifying which environmental, social, and governance topics matter most to your business and to the people and ecosystems it affects. The output is a prioritised list of material issues that shapes your sustainability strategy, your ESG KPIs, and your regulatory disclosures.

Think of it as the sustainability equivalent of a financial risk register — except instead of asking only “what could hurt our balance sheet?”, it also asks “what impact are we having on the world?”

Both questions, for companies in scope of the Corporate Sustainability Reporting Directive, now carry formal reporting obligations.

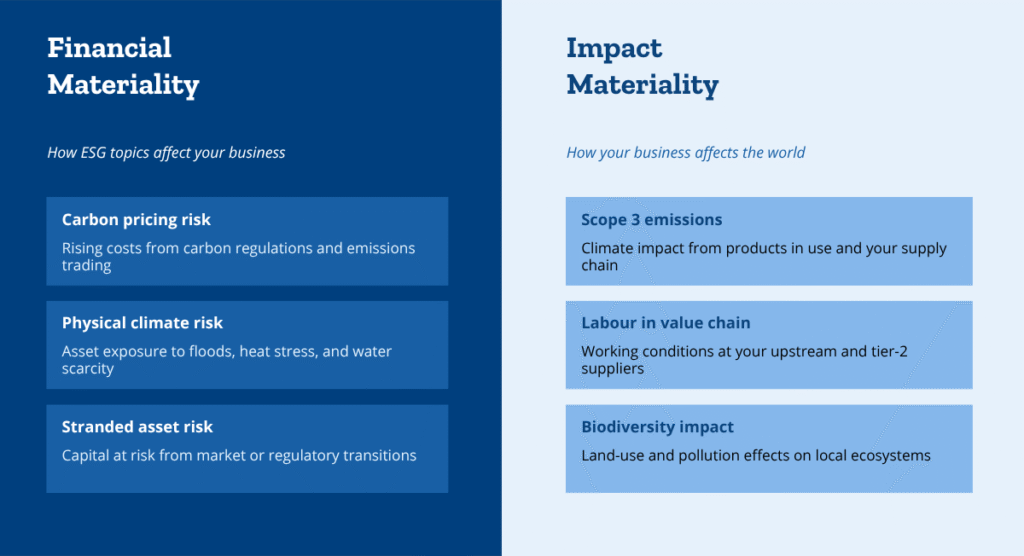

Financial vs. Impact Materiality: The Double Materiality Concept

Not all ESG topics carry the same weight for every business. A materiality assessment is how you determine which ones do — and from which direction. Some topics are material because of what they could do to your business. Others are material because of what your business does to the world. The double materiality concept captures both.

We cover this in detail in the next section, but it is worth establishing early: The distinction between financial and impact materiality is the defining feature of the European approach to sustainability reporting, and it shapes everything that follows in this process.

Why It Is Now the Basis for ESRS Reporting for In-Scope Companies

The Corporate Sustainability Reporting Directive established the double materiality assessment as the basis for ESRS reporting for in-scope companies. Rather than leaving companies to decide what to report and why, the CSRD requires every in-scope company to first demonstrate which sustainability topics are material — and to document how that conclusion was reached.

This shifts materiality from a best-practice exercise to a compliance obligation with audit implications. A materiality assessment is no longer something you do because it looks good in an annual report. It is the foundation that every ESRS disclosure sits on.

Double Materiality Assessment: Financial Materiality vs. Impact Materiality Explained

Financial Materiality: ESG Risks That Affect Company Value

Financial materiality asks: How do sustainability topics affect our business? This covers risks to revenue, asset value, cost structures, and access to capital. Physical climate risk to manufacturing facilities. Carbon pricing risk to operational margins. Water scarcity risk to production continuity.

These are the sustainability risks that can move your company’s financial performance — and they map closely to how your enterprise risk management function already evaluates risk. If your ERM team speaks this language, bring them in early. It avoids duplicating effort and strengthens both processes.

Impact Materiality: Your Company’s Effect on Environment and Society

Impact materiality asks: How does our business affect the environment and society? This covers actual and potential negative — and positive — impacts across your own operations and your entire value chain. Scope 3 emissions from products in use. Labour conditions at tier-two suppliers. Biodiversity loss from upstream land-use decisions.

The key difference from financial materiality is directionality. Impact materiality is inside-out: it is about what you do to the world, not what the world does to your numbers. For many companies, this lens surfaces issues that have never appeared on a risk register — which is precisely why the CSRD mandates it.

ESRS Requirement: Both Perspectives Must Be Assessed

Under the European Sustainability Reporting Standards, a sustainability topic can be material from one perspective, the other, or both simultaneously. The specific disclosure requirements this triggers will depend on which topics are assessed as material and which ESRS topical standards apply to them — the depth and scope of reporting varies by topic and standard.

This is not a choice between financial and impact. It is a requirement to assess both, document your conclusions for each, and let those conclusions determine which areas of the ESRS your organisation must report against.

The Corporate Sustainability Reporting Directive and the European Sustainability Reporting Standards: What They Actually Require

The CSRD and its accompanying European Sustainability Reporting Standards represent the most significant structural shift in corporate sustainability reporting the EU has introduced. The double materiality assessment is not an optional input to your sustainability report — it is the document that determines what your sustainability report must contain.

The CSRD’s mandatory scope and implementation timeline have been subject to ongoing refinement through the EU’s Omnibus simplification process. The thresholds for mandatory applicability have been raised, significantly narrowing the number of companies initially required to report.

For the most current scope criteria and applicable thresholds, we recommend checking the European Commission’s official CSRD page, as these details continue to be updated as final legal texts are confirmed.

If your organisation falls outside mandatory scope, conducting a materiality assessment is still strongly advisable. Investors, lenders, and the larger companies in whose supply chain you sit are increasingly requesting ESG disclosures as a standard condition of doing business regardless of your regulatory obligation.

A note on the evolving ESRS: EFRAG has published revised draft standards and implementation guidance, including proposed simplifications around biodiversity (ESRS E4) and value chain data requirements (ESRS S2 to S4). The adoption timeline and which reporting periods will apply which version of the standards are subject to ongoing confirmation.

EFRAG’s Sustainability Reporting Board Chair Chiara Del Prete breaks down the latest regulatory developments.

We recommend checking EFRAG’s official resources and the European Commission’s CSRD page for the most current status before making reporting decisions based on version-specific requirements.

When and How Often Should You Conduct a Materiality Assessment?

Initial Assessment vs. Annual Review

The first time you conduct a materiality assessment, it is a full-scope exercise. For a large organisation running a rigorous process, this typically takes three to six months. It covers stakeholder mapping, topic identification against ESRS, scoring, matrix development, and governance sign-off at board or senior management level.

After that initial assessment, ESRS 1 expects companies to review their materiality conclusions each reporting year — but this does not mean repeating the full process. It means assessing whether the landscape has shifted: new regulatory requirements, emerging ESG risks, operational changes, or stakeholder feedback that would alter your conclusions. Document your reasoning either way. The annual review is part of the audit trail.

Triggers for an Ad Hoc Reassessment

Certain events should prompt you to revisit your materiality conclusions outside the annual cycle:

- A significant acquisition or disposal that changes your operational footprint or sector exposure

- Entry into a new geography or market with different regulatory or environmental conditions

- A major regulatory development in one of your operating markets

- A material incident — environmental, social, or governance — that surfaces new risks or impacts

- Significant shifts in investor or supply chain expectations around specific ESG topics

If any of these apply, the conclusions from eighteen months ago may no longer reflect your actual risk and impact profile.

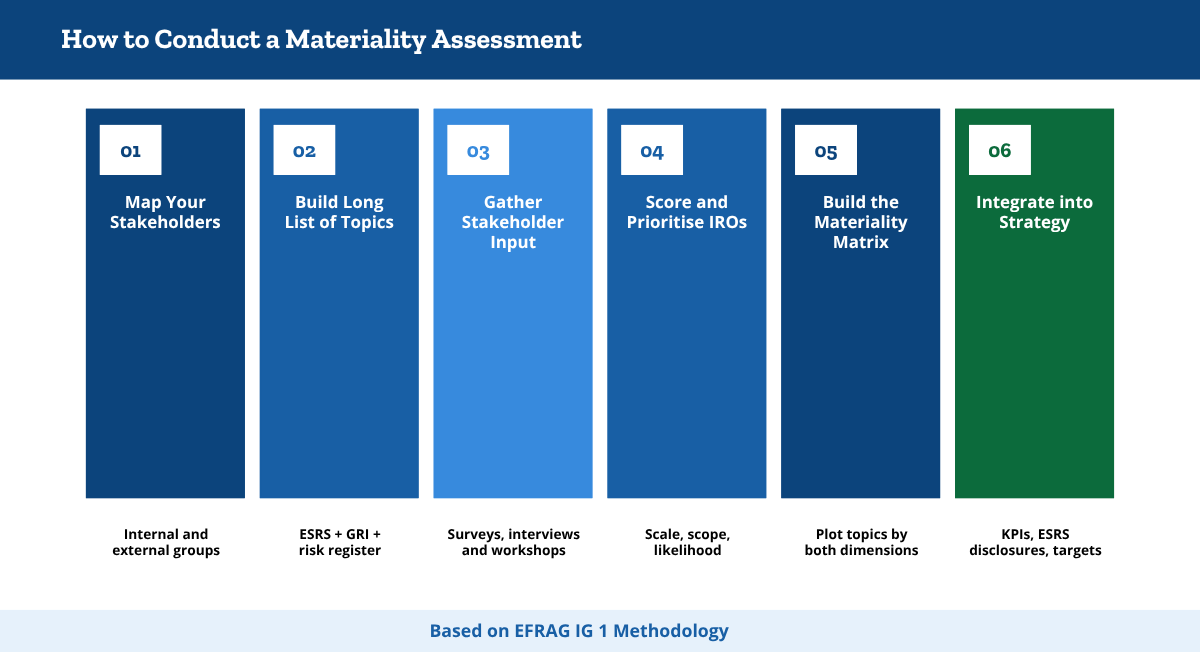

How to Conduct a Materiality Assessment: Six Steps That Hold Up Under Audit

Step 1: Map Your Key Stakeholders

Start by mapping who has a stake in your business and who your business has an impact on. These are not the same list — and conflating them is one of the most common design errors in the materiality assessment process.

The first group — those with a stake in your business — includes investors, lenders, customers, employees, and key suppliers. The second group — those affected by your activities — includes communities near your operations, workers across your value chain, and the natural environment where your activities leave a footprint.

ESRS 1 distinguishes between “affected stakeholders” and “users of sustainability statements” — both groups need representation in the process. Focusing only on investor-facing stakeholders produces an assessment skewed toward financial materiality and blind to impact-side topics that could surface later as regulatory or reputational exposure.

In practice: assign internal ownership for each stakeholder group before designing any outreach. Decide which groups will be engaged directly and which will be assessed through secondary research. This decision, and the rationale behind it, is part of your audit trail.

Step 2: Develop a Long List of ESG Topics

Before you can prioritise, you need a comprehensive starting inventory. Build it from multiple sources simultaneously not sequentially.

ESRS 1 provides the reference framework, mapping across topical ESRS areas: climate change, pollution, water and marine resources, biodiversity and ecosystems, circular economy, own workforce, workers in the value chain, affected communities, consumers and end-users, and business conduct. Not all will be material for every company, but all should be evaluated at this stage.

Cross-reference with GRI Universal Standards and, where relevant, SASB standards for your sector — these provide benchmarks on what is typically material for companies of your type.

Also draw from internal sources: Your risk register, incident logs, existing ESG data, and any prior sustainability reports. Your long list at this stage may contain 30 to 60 topics. That is expected. The purpose of subsequent steps is to narrow it systematically, not arbitrarily.

Step 3: Prioritise Through Stakeholder Engagement (Surveys, Workshops, Interviews)

This is the step where external perspectives formally enter the process — and where the quality of your methodology will either stand up or quietly fall apart under scrutiny.

Most organisations use a combination of surveys, structured interviews, and workshops. Surveys work well for employees and customers at scale. Structured interviews suit institutional investors, regulators, and community representatives where depth matters more than volume. Workshops work well for internal stakeholders — senior management, legal, finance, and sustainability teams — where the goal is to surface business context and test assumptions.

A few design errors that will undermine this step:

- Sending a 60-topic survey to key investors and expecting substantive responses

- Using the same instrument across every stakeholder group regardless of their relationship to your business

- Treating ranked outputs as final materiality conclusions without applying business judgment

Stakeholder engagement is a critical input to the process. It is not the process itself. Document methodology, response rates, and how input was weighted. This documentation will be reviewed in assurance.

Step 4: Assess Business Impact (Probability and Magnitude of Financial and Impact Risks)

For each topic on your long list, apply a scoring methodology that captures both dimensions of materiality — and define your scoring criteria before you begin, not after.

For financial materiality, assess:

- Probability of occurrence

- Magnitude of financial effect on revenues, costs, assets, or liabilities

- Time horizon across short, medium, and long term

For impact materiality, assess:

- Severity of impact — which ESRS 1 breaks down into scale, scope, and remediability

- Whether the impact is actual or potential

- Whether it occurs in your own operations or across your value chain

Deciding what “high” means retrospectively is how assessments accumulate the appearance of rigour without the substance. Set thresholds first, apply them consistently, and document the basis for every score.

Where data arrives from diverse sources — supplier submissions, utility invoices, certificates, third-party disclosures — a system that consolidates and validates those inputs against your material topics keeps the process traceable and defensible, rather than held together by a spreadsheet and institutional memory.

Scoring value chain impacts requires “supplier data” and most companies don’t have it yet.

If Scope 3 or supply chain conditions are appearing on your long list, the groundwork for acing them starts with structured supplier outreach. Our Scope 3 Supplier Engagement Workbook helps you collect, validate, and organise that data before it feeds into your materiality scores.

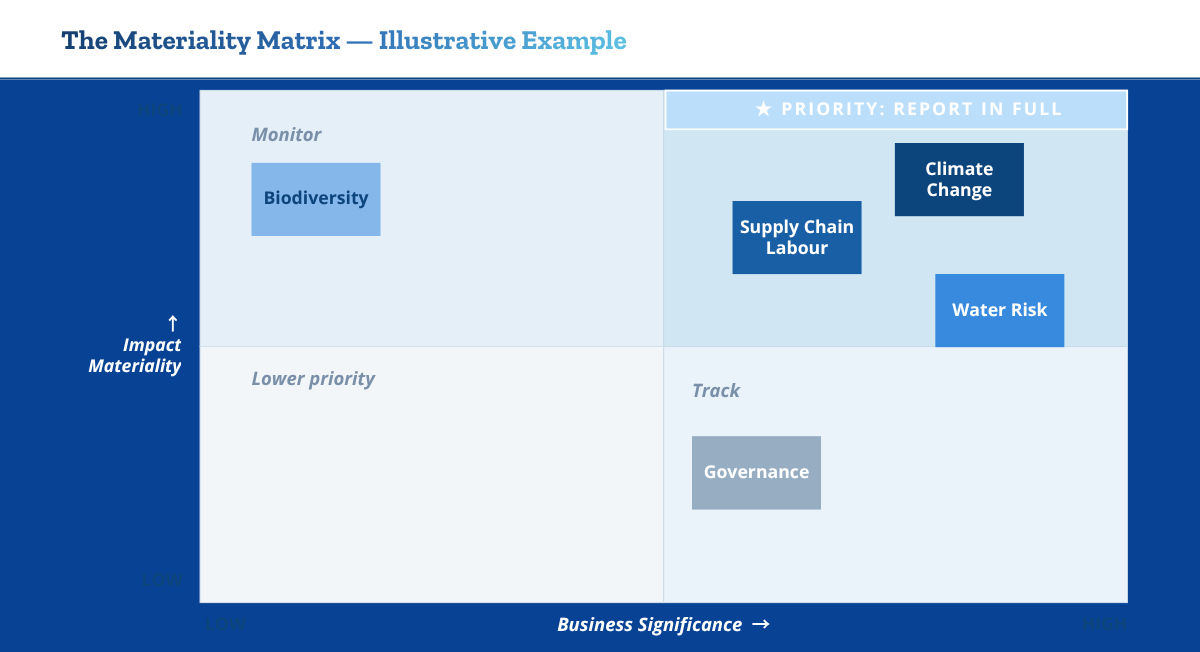

Step 5: Create the Materiality Matrix (Plotting Topics by Relevance to Business and Stakeholders)

The materiality matrix is an essential component of any robust materiality assessment and its standard visual output. It plots material ESG topics on a two-axis grid, with business significance on one axis and stakeholder expectations on the other. Topics in the upper-right quadrant are your material sustainability topics — the issues that enable companies to allocate resources effectively and direct sustainability efforts where they matter most.

To be precise about what the matrix is and what it is not: The materiality assessment process determines which topics are material for your organisation. The matrix is the visual summary of those conclusions. It helps communicate which topical ESRS areas are relevant for your company’s reporting — but the underlying assessment and documentation is what carries regulatory weight.

If climate is assessed as material, you report against ESRS E1 in full — targets, transition plans, and scenario analysis included. If biodiversity is assessed as not material, you may omit ESRS E4, but you must document your reasoning clearly.

Every topic below your materiality threshold needs a documented rationale. “We assessed it and it did not meet our defined threshold” is defensible. “We didn’t look at it” is not — and auditors are very good at telling the difference.

Note: The European Sustainability Reporting Standards (ESRS) do not mandate a specific visual format for the matrix. What regulators and assurance providers scrutinise when conducting materiality assessments is the documented process behind it i.e. how relevant stakeholders were engaged through structured stakeholder dialogue, how topics were scored in assessing impacts and determining materiality, and how governance sign-off was obtained.

Step 6: Integrate Into Strategy and Reporting (Using the Matrix to Prioritise ESG KPIs and Disclosures)

This is where most organisations lose the value they spent months building. The matrix gets completed, validated by the board, placed in the sustainability report, and largely ignored until the following year.

Beyond being a missed opportunity, this is increasingly a credibility risk. Investors and assurance providers are asking a direct question: how did your material topics actually influence your strategic decisions? If supply chain conditions ranked as high-priority in your assessment but your procurement policy is unchanged, that gap will attract scrutiny.

Meaningful integration looks like this:

- Material topics map to ESG KPIs with defined owners, targets, and reporting cycles

- Strategic decisions on capital allocation, supplier qualification, and product development reference materiality conclusions

- The sustainability report shows — not merely asserts — how material topics shaped strategy

Under ESRS, companies must explain how their material impacts, risks, and opportunities connect to business strategy and governance. This is a disclosure requirement, not optional narrative. Systems that link your material topics to data collection, performance tracking, and reporting workflows make that traceability significantly easier to sustain — and significantly harder for auditors to question.

Materiality Assessment Under CSRD: What’s Required?

ESRS 1 Requirements for Double Materiality

ESRS 1 sets the general requirements for the double materiality assessment process itself. It establishes how companies must approach the identification of impacts, risks, and opportunities — referred to throughout the standards as IROs — and how those conclusions flow into the selection of ESRS topics for disclosure.

Key requirements under ESRS 1 include:

- Documenting the process used to identify IROs across your own operations and value chain

- Explaining how stakeholders were identified and how their perspectives were incorporated

- Disclosing which ESRS topics were assessed as material and providing clear reasoning for any topics assessed as not material

- Ensuring governance sign-off at board or senior management level

ESRS 2 then translates these conclusions into specific disclosures — particularly under IRO-1 (process for identifying IROs), IRO-2 (mapping of IROs to ESRS disclosure requirements), and SBM-3 (material impacts, risks, and opportunities and their interaction with strategy). These are structured disclosures with an evidence base behind them, not summary paragraphs.

Documentation, Audit Trail, and Assurance

CSRD compliance does not begin with disclosure. It begins with documentation.

Every scoring decision, stakeholder input, and governance sign-off must be traceable. The materiality assessment process must be defensible, consistently applied, and reproducible — which means moving away from approaches where the methodology lives in one person’s head and the evidence lives in an email thread.

Under CSRD, sustainability information is subject to external assurance, and the materiality assessment process and its documentation fall within scope of that engagement. Assurance providers will ask to see how topics were scored, who was consulted, what thresholds were applied, and how the final list of material topics was derived.

The audit trail is not a bureaucratic afterthought. It is the product. An assessment without a structured, queryable evidence base is not assurance-ready — regardless of how sound the underlying conclusions are.

Tools That Help You Run an ESG Materiality Assessment Without Losing the Thread

Running a materiality assessment manually — through spreadsheets, email surveys, and shared document folders — is workable for a small organisation doing a first pass. For a large organisation with complex operations, multiple geographies, and formal assurance requirements, it introduces significant process risk.

The predictable failure points: stakeholder input that cannot be traced to source; scoring applied inconsistently across reviewers; documentation that does not meet auditor expectations; institutional knowledge that walks out the door when a key team member leaves. None of these are hypothetical — they are the most common reasons assessments fail assurance review.

Datamaran automates the identification of relevant ESG topics and material ESG issues through regulatory and media monitoring, useful at the topic scanning phase when companies decide which sustainability matters to include in their long list. Workiva provides financial-grade reporting infrastructure and audit tooling, helping organisations track and disclose sustainability performance across ESG and financial data.

Credibl is built around a different premise: That the materiality assessment is not the end of the process, but the beginning of it. The platform consolidates structured and unstructured data — supplier inputs, utility invoices, certificates, third-party disclosures — into a single system of record, with AI-powered ingestion and validation designed to support structured, traceable data management. Material topics connect directly to data collection workflows, KPI tracking, and ESRS-aligned disclosure preparation, with evidence linking and structured control workflows designed to support the traceability that assurance requires.

How Software Streamlines Stakeholder Engagement and Analysis

The right technology choice depends on where your biggest process risk sits. If identifying and monitoring emerging material topics is the bottleneck, a regulatory intelligence tool helps most. If documentation, audit trail, and multi-framework disclosure are the constraint, a unified platform is the higher-value investment.

What good software should do — at minimum — is eliminate the version control problem, standardise the scoring methodology, and produce documentation that can be handed to an assurance provider without a week of preparation.

The result, when technology and process are aligned, is a sustainability data backbone that supports reporting across CSRD, IFRS S1/S2, and other frameworks without rebuilding the process from scratch for each one.

Credibl helps sustainability teams…

… move from materiality assessment to CSRD-ready reporting with structured data collection, ESRS alignment, and documentation built in, from day one.