If your company has pledged to reach net zero, you are in good company. Most large organisations have made some version of that commitment. The harder question is whether there is a real plan behind it.

A decarbonisation strategy is not a pledge. It is the architecture that turns ambition into a structured, measurable, and auditable programme — one that maps actual carbon emissions to time-bound targets, assigns accountability to specific reduction levers, and can hold up under scrutiny from regulators, investors, and auditors alike.

This guide walks you through every step: what to measure, how to set emission reduction targets that will survive scrutiny, which levers to prioritise, and how to report in a way that builds credibility. Think of it as the practical companion to the net zero commitment your board has already made.

What is a decarbonisation strategy?

A decarbonisation strategy is a structured, time-bound plan for reducing — and ultimately eliminating — your company’s greenhouse gas emissions across all areas of operation and your wider value chain.

It is not the same as carbon neutrality. Carbon neutrality can technically be achieved by purchasing carbon credits to offset what you emit, without changing a single process in your business. Decarbonisation requires actual carbon reduction at source. Regulators, science-based target frameworks, and increasingly investors are focused on the latter, not the former.

The link to the Paris Agreement is direct. Limiting global warming to 1.5 degrees Celsius requires corporate emissions to fall substantially by 2030. That does not happen through tree planting and offset purchases alone. It requires genuine emissions reduction across operations and supply chains at a scale that only a structured strategy can deliver.

It is also worth distinguishing a decarbonisation strategy from a transition plan. A transition plan — as required under CSRD’s ESRS E1 — is the formalised, disclosed version of your strategy. The strategy is the thinking, data infrastructure, and operational work that makes the plan credible. One without the other tends to show, particularly when auditors get involved.

Why your business needs a decarbonisation strategy?

The case for a corporate decarbonisation plan has shifted considerably. It is no longer primarily about brand reputation or environmentally conscious consumers though both remain real. It is about regulatory exposure, cost competitiveness, and access to capital.

Regulatory pressure

For European companies, CSRD is the most immediate driver. Large companies with more than 1,000 employees must disclose a climate transition plan aligned to 1.5 degrees Celsius — or explain in their annual report why they do not have one. The EU Omnibus Package (April 2025) narrowed CSRD’s scope and extended certain deadlines. What it did not do is remove the transition plan requirement for companies that remain in scope. The delay has reduced urgency for some; it has not reduced the obligation.

CBAM cost exposure

The Carbon Border Adjustment Mechanism currently covers cement, steel, aluminium, fertilisers, electricity, and hydrogen imported into the EU. The European Commission is reviewing CBAM’s scope in the second half of 2025, with legislative changes expected in early 2026 including potential expansion to additional sectors.

For any company importing from or competing with carbon-intensive supply chains, reduce emissions is no longer just a reporting question. It is a cost management one.

As Ashwin J, ESG Manager at Credibl, puts it:

“CBAM is transforming carbon emissions from a sustainability metric into a trade and competitiveness issue. One of the key challenges in CBAM implementation is establishing accurate product-level emissions calculations when energy, material consumption, and emissions data are typically available only at facility or process levels. Organisations exporting to the EU must therefore develop robust allocation methodologies and maintain auditable, transparent data to accurately report embedded emissions and meet evolving regulatory requirements. Companies that build strong carbon accounting capabilities can improve transparency, strengthen customer confidence, and enhance their competitiveness in low-carbon markets.”

Investor and lender expectations

Frameworks like TCFD and ISSB’s IFRS S1/S2 are moving from voluntary best practice to expected standard. Banks and institutional investors across Europe are tying financing terms to verified emissions data and credible reduction pathways. A net zero strategy built on unverifiable estimates will not survive lender due diligence for long.

Consumer demand and supply chain requirements

Consumer demand for transparency is rising, and so is supply chain pressure. Large companies are increasingly requiring their suppliers to measure and disclose emissions as a condition of doing business. If your major customers are building their own Scope 3 programmes, your carbon footprint will eventually appear in someone else’s disclosure — whether you have measured it accurately or not.

Step 1: Measure your carbon footprint

You cannot manage what you have not measured — and in carbon accounting, measurement quality determines everything that comes after it.

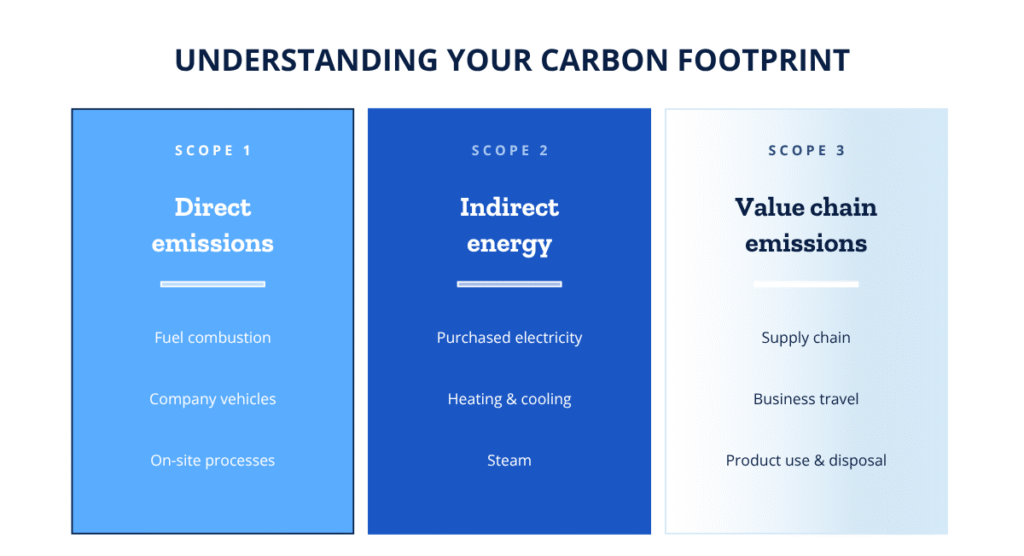

The starting point is a complete GHG emissions inventory across all three scopes, calculated using the GHG Protocol Corporate Standard. This is the globally accepted framework for measuring, reporting, and managing greenhouse gas emissions, and the methodology recognised by SBTi, CSRD, CDP, and most investor frameworks.

Scope 1 covers direct carbon emissions from sources your company owns or controls — combustion in boilers and vehicles, on-site industrial processes, fugitive refrigerant releases. These are the most straightforward to measure and typically the first to be addressed.

Scope 2 covers indirect emissions from purchased electricity, steam, heat, and cooling. It can be calculated using a location-based method (grid average emissions factors) or a market-based method (contractual instruments like renewable energy certificates). The method affects your reported number materially and must be applied consistently year on year.

Scope 3 is where most companies’ carbon footprint actually lives — upstream from suppliers, downstream from the use and disposal of your products. It typically represents the largest share of total emissions.

And most Scope 3 data problems start with supplier engagement.

The three calculation methods

Three approaches are available for Scope 3, each with different accuracy and effort implications:

- Spend-based: Financial spend data multiplied by industry-average emissions factors per unit of spend. Fast to apply, useful for initial screening, but low accuracy.

- Activity-based: Physical quantities — tonnes of materials, kilometres travelled — multiplied by published average emissions factors. More accurate for direct operations and higher-spend categories.

- Supplier-specific (primary data): Actual emissions data collected directly from suppliers. Highest accuracy, most defensible under audit, and required for credible science-based target validation in material categories.

Most companies start with spend-based for screening, activity-based where physical data is available, and build out supplier-specific data over time for the highest-impact categories.

Setting a base year

The base year anchors your carbon reduction targets and all future progress comparisons. It should be the most recent full year for which you have reliable, complete data. Choose it carefully — changing it later requires a documented restatement.

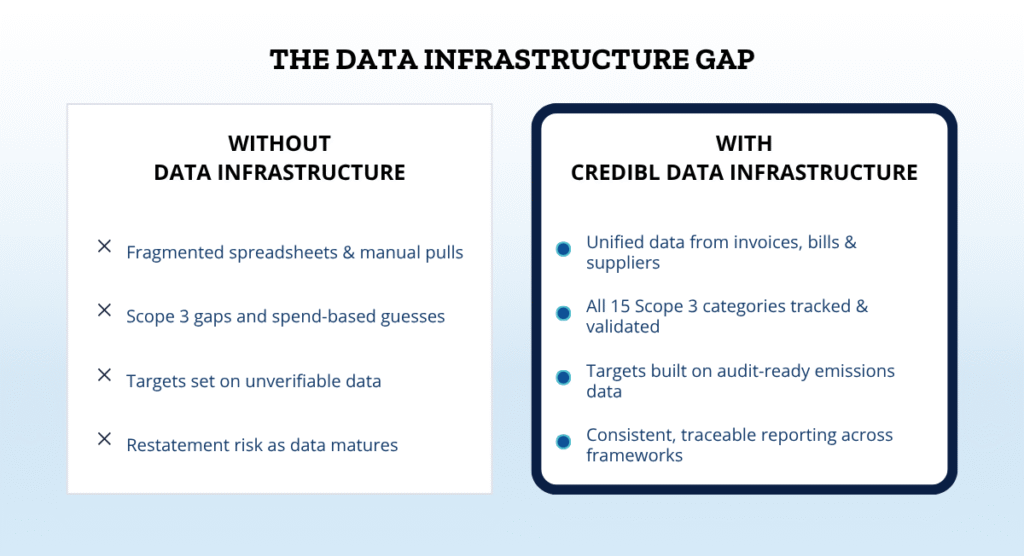

The quality of this baseline determines everything downstream. Emissions calculations built on fragmented spreadsheets and manual data pulls create restatement risk as data quality improves and the actual footprint diverges from what was originally reported. Automating data ingestion from source documents — invoices, utility bills, supplier disclosures — directly into a validated system of record materially reduces that risk from the outset.

Step 2: Set science-based targets

With a defensible baseline in place, you can set ambitious targets that will hold up.

The Science Based Targets initiative (SBTi) is the most widely recognised framework for corporate target setting. SBTi-validated targets are aligned to the 1.5°C pathway under the Paris Agreement, independently verified, and used by investors, procurement teams, and CDP as a proxy for the credibility of a company’s net zero strategy.

Near-term targets require significant absolute reductions by 2030, covering Scope 1 and 2 and — for companies where Scope 3 exceeds 40% of total emissions — Scope 3 as well. Long-term (net zero) targets require at least a 90% absolute reduction across all scopes by 2050, with residual emissions addressed through permanent carbon removal, not conventional offsets.

The updated SBTi Corporate Net-Zero Standard (Version 2.0) places greater emphasis on absolute reductions at source. The expectation is direct carbon reduction — not creative accounting through offsets.

Sector-specific pathways matter. A manufacturing business faces different decarbonisation pathways than a financial institution or a logistics provider. SBTi provides sector-specific guidance to ensure targets are credible for your industry context, not just for the climate science. It is worth reviewing sector pathways before finalising your net zero target.

Despite the fact that Scope 3 often represents 75–90% of a company’s total carbon footprint, only a small minority of companies have validated science-based Scope 3 targets, and an even smaller fraction are currently on track to meet them, according to recent analyses of SBTi data.

That is not primarily an ambition problem. It is a data problem. Ambitious targets set on top of spend-based Scope 3 estimates carry restatement risk when data matures. Getting the data infrastructure right before locking in targets is not over-caution — it is how you avoid a damaging correction two years in.

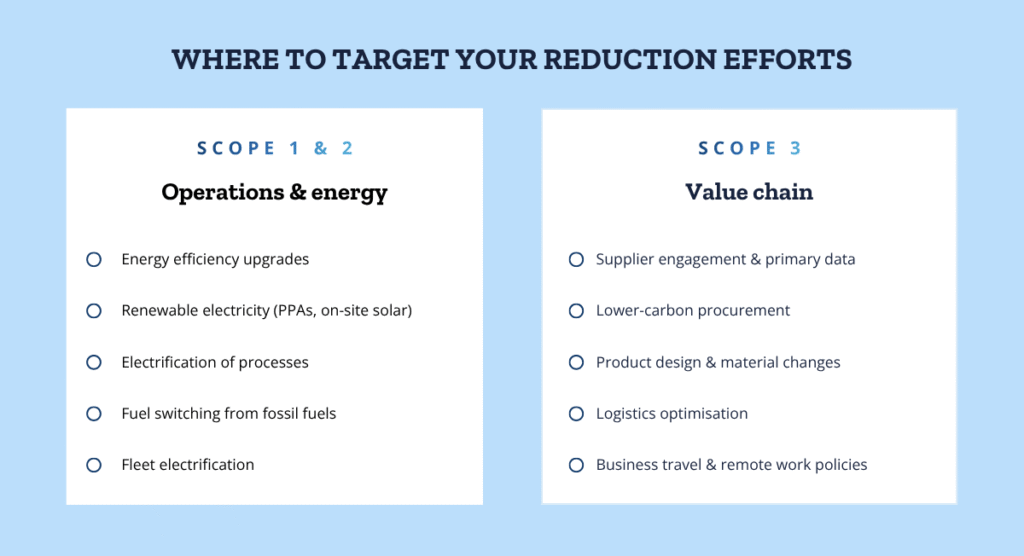

Step 3: Identify reduction levers

This is where strategy meets operation. Identifying the right decarbonisation pathways for your business requires knowing where your emissions are concentrated and which levers can realistically move numbers within your planning horizon.

Energy efficiency

Energy efficient practices are usually the fastest lever and the one with the strongest return on investment. Building retrofits, smart metering, LED lighting upgrades, and HVAC optimisation can move Scope 1 and Scope 2 numbers meaningfully while reducing energy costs.

The logic is simple: energy you do not consume is energy you do not need to decarbonise. It is the kind of result a CFO appreciates even before the carbon argument is made. Process audits of facilities and equipment — often underused — frequently surface efficiency opportunities that have been invisible simply because no one was looking for them.

Renewable energy transition

Switching to renewable energy sources directly reduces your market-based Scope 2 emissions. The main routes are Power Purchase Agreements (PPAs) with renewable generators, on-site solar or wind installation, and Renewable Energy Certificates (RECs).

In the European context, corporate PPAs are increasingly available and competitively priced. A well-structured PPA can eliminate Scope 2 exposure while providing longer-term energy price stability — a hedge against both carbon pricing and market volatility. Power generation through on-site renewables adds an additional layer of resilience for energy-intensive operations.

Process innovation

For companies in carbon-intensive sectors, deeper change is required — electrification of industrial processes, fuel switching away from natural gas and fossil fuels, adoption of low carbon technologies, and circular economy design that reduces raw materials consumption and waste disposal emissions.

These interventions require longer planning horizons and more capital than efficiency measures. They also represent the largest reduction potential for heavy industry and the hardest categories to decarbonise. Internal carbon pricing — assigning a shadow cost to carbon in investment decisions — makes the business case for process change significantly easier to construct.

Supply chain engagement

Supply chain decarbonisation is, in the honest assessment of most sustainability leads, the hardest part of the whole programme. It requires meaningful action from third parties — your suppliers — over whom you have influence but not direct control.

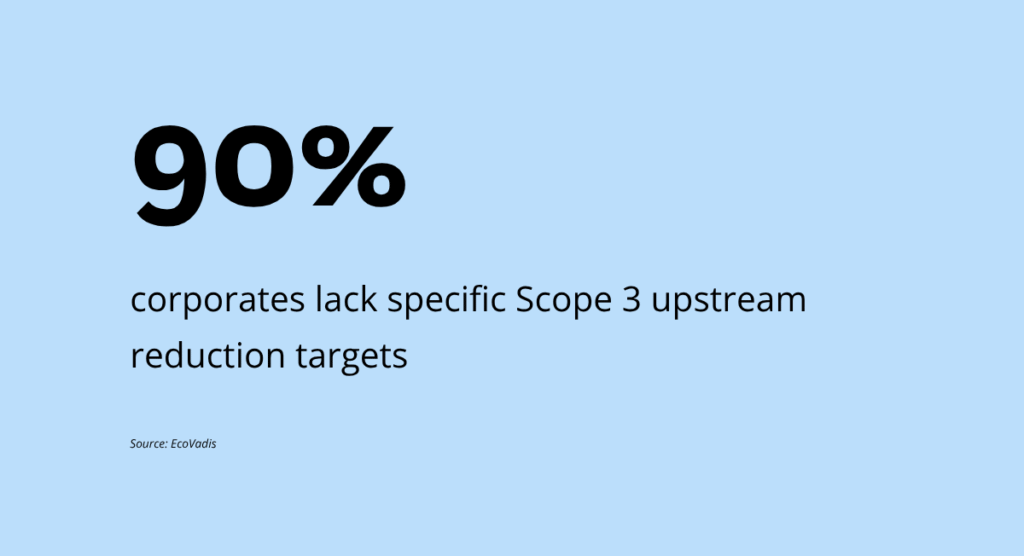

Research by EcoVadis shows that over 90% of companies have no specific Scope 3 supply chain reduction targets in place. Only one in three actively engages their suppliers on climate action. The result is that for most companies, the largest share of total emissions sits largely unaddressed.

The most effective approach is to tier suppliers by emissions impact first. Identify which spend categories and which specific suppliers account for the majority of your upstream Scope 3 footprint, and direct engagement there. Collecting primary emissions data from high-impact suppliers — rather than relying indefinitely on spend-based estimates — is the step that most meaningfully improves target credibility and closes the data gap.

Platforms that can run supplier assessments, validate evidence, and pull in data automatically from public disclosures reduce the operational burden of this work — turning supplier engagement from a spreadsheet exercise into a systematic programme.

Business travel and commuting

Business travel and employee commuting tend to receive more attention than their emissions share warrants for most organisations — but they matter for two reasons. They are measurable, which makes them useful for demonstrating early progress. And they are visible internally, which helps build organisational structure around climate action more broadly.

Remote work policies, electric vehicle fleet transitions, and sustainable travel guidelines are the primary levers. For most businesses, these are not the largest contributors to the total carbon footprint — but they are among the most straightforward to act on, and they build the internal muscle needed for the harder supply chain work ahead.

Step 4: Implement and monitor progress

A carbon reduction plan without a monitoring framework will drift. Execution requires KPIs, milestones, and clear ownership — treated with the same discipline applied to financial performance tracking.

Set quarterly reviews. Annual reporting cycles are too slow to catch course corrections before they become material problems. Quarterly reviews of progress against decarbonisation targets by scope and category — with named accountability for each reduction lever — create the rhythm that makes plans survive operational reality.

Assign ownership at the operational level. Every lever needs a named owner, not the sustainability team in aggregate, but a specific business unit leader, supply chain manager, or facility head with accountability for delivery. Decarbonisation that lives entirely within the sustainability function will not scale across the organisation.

Use internal carbon pricing. Assigning a shadow price to carbon emissions across business units changes investment decisions around energy, travel, procurement, and process design. It does not require a formal internal market — even a requirement that capital expenditure proposals include a carbon cost estimate shifts the conversation.

Carbon management software that consolidates emissions data from operations, utilities, suppliers, and finance in real time replaces the quarterly scramble of manual data aggregation. When your data infrastructure is connected and validation happens upstream of reporting — not during it — your progress metrics are reliable enough to act on, not just to publish. That is the difference between a monitoring capability and a compliance exercise.

Step 5: Report and communicate progress

Reporting is not the end of a decarbonisation strategy. It is the accountability mechanism that makes everything before it credible — and the point at which data quality problems that have been quietly managed internally will surface publicly.

Annual sustainability reporting aligned with CSRD/ESRS, GRI, and TCFD standards provides the structured disclosure framework that investors, regulators, and major customers expect. For companies within CSRD scope, ESRS E1 requires: disclosure of the transition plan (or an explanation of its absence), gross Scope 1, Scope 2, and Scope 3 emissions broken down by category, quantified reduction targets with base year and methodology, and the capital expenditure allocated to fund the transition plan. This is updated annually — it is a recurring disclosure, not a one-time document.

CDP disclosure is voluntary but effectively expected across the European investment and procurement community. Institutional investors and large buying organisations use CDP scores as a standard signal for climate impact management maturity. Absence from CDP, or a weak score, is read as a signal — often more clearly than companies realise.

Stakeholder communication beyond formal disclosure matters too. A “do once, report many” approach — where the same validated underlying dataset produces CSRD outputs, CDP responses, investor briefings, and customer-facing disclosures — ensures consistency and removes the duplication that comes from managing multiple parallel reporting processes. Consistency across disclosures is not just efficient. It is a credibility signal in itself.

Common barriers and how to overcome them

Organisational misalignment

The most common reason decarbonisation plans stall is internal rather than external. Without board-level ownership and cross-functional accountability, sustainability goals sit with the sustainability team and go no further. The fix is structural: decarbonisation targets need to be embedded in capital planning, procurement criteria, and performance reviews — not managed as a parallel programme that competes for attention with the core business.

Board buy-in is easier when the frame is right. This is a regulatory compliance issue, a cost exposure management exercise, and a risk mitigation programme — not a values statement. Present it accordingly.

Data gaps in Scope 3

Scope 3 data gaps are near-universal and genuinely difficult. The answer is not to wait until data is perfect — it never will be. Start with what you have, document your methodology transparently, and build a roadmap for improving data quality over time.

Supplier engagement frameworks that tier by emissions impact, prioritise primary data collection for the highest-emission categories, and use automated data augmentation from public disclosures to fill gaps where direct data is unavailable — these are the practical tools that close the gap progressively. Transparency about where your data is strong and where it is estimated builds more credibility than silence.

Budget constraints

The ROI case for decarbonisation investment is stronger than most finance teams initially assume. Energy efficiency measures typically recover costs within a few years. Renewable energy PPAs can reduce and stabilise energy costs over a contract term. And the cost of non-compliance — regulatory penalties, audit exposure, investor downgrade, supply chain exclusion — is rarely factored into the “this is too expensive” objection.

The companies that will face the steepest costs are not those that invested early. They are those that delayed and then had to reconstruct years of GHG data under audit pressure, with inadequate systems and very little time.

Building a decarbonisation strategy that holds up

A corporate decarbonisation strategy is only as credible as the data underneath it. Ambitious targets matter. The infrastructure to deliver, monitor, and verify them matters more.

The key components of a strategy that holds up are: a defensible, version-controlled baseline; science based targets validated against the 1.5°C pathway; a prioritised lever portfolio with operational ownership; and reporting architecture that produces consistent, auditable outputs across frameworks.

Credibl helps organisations build exactly that — a unified sustainability data backbone that consolidates structured and unstructured data from invoices, utility bills, supplier disclosures, and certificates into a single, audit-ready system. With AI-powered ingestion and validation, Scope 3 and supply chain coverage, and integrated reporting across CSRD/ESRS, IFRS S1/S2, and TCFD — it is designed for companies that need to stay ahead of regulatory expectations, not catch up to them.

If you are building or revising your carbon reduction plan, see where your current data gaps are.