Every quarter, another company discovers that what it dismissed as a sustainability issue was, in fact, a financial one.

The Volkswagen diesel emissions scandal is estimated to have cost the company approximately €30 billion in total since 2015, including fines, buybacks, recalls, and legal settlements. BP’s Deepwater Horizon disaster resulted in one of the largest corporate environmental settlements on record — a 2016 settlement with the US government and five states reaching $20.8 billion — with total spill-related costs for BP exceeding $60 billion by mid-2016.

Neither happened because the risk was invisible. Both happened because poor ESG risk management allowed known exposures to compound unchecked until they became catastrophic.

ESG risk is now a mainstream financial concern, not a values exercise. Regulatory bodies, investors, and lenders are pricing it accordingly. The European Banking Authority published its Guidelines on the Management and Supervision of ESG Risks for credit institutions and investment firms, applicable from 11 January 2026 for institutions subject to CRD 6, and from 11 January 2027 for small and non-complex institutions, requiring financial institutions to integrate environmental, social, and governance factors into their credit assessment and risk management processes.

Whether you are building an ESG risk framework from scratch or pressure-testing an existing one, this blog covers the full picture.

Here’s what you will walk away with:

- Why ESG risk is not the same as ESG performance, and where the real exposure sits in your business.

- The three categories of ESG risk: Environmental (physical and transition), social, and governance, and why each requires a different management approach.

- Why ESG risk behaves differently from traditional financial risk: Longer time horizons, harder-to-quantify data, and systemic industry-wide exposure.

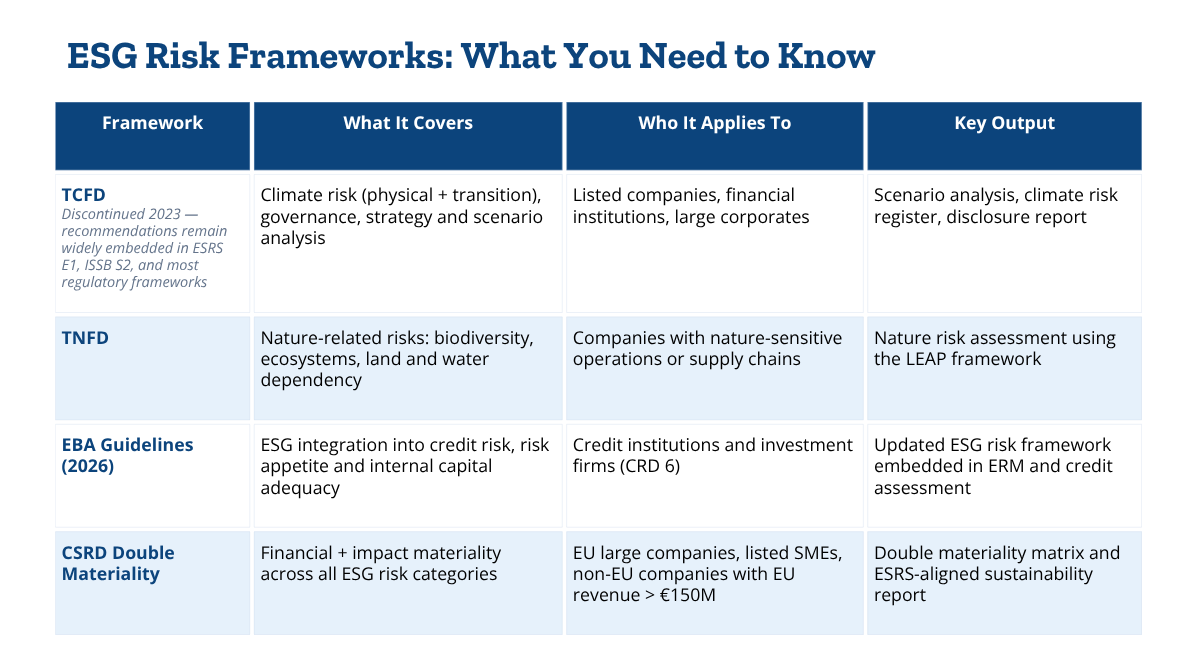

- The four frameworks that define current best practice: TCFD, TNFD, EBA Guidelines from January 2026, and CSRD double materiality.

- A five-step process for building an ESG framework that sits inside enterprise risk management, not parallel to it.

- The current CBAM timeline including the transitional reporting in force since October 2023 (full financial mechanism starts 1 October 2026).

- The ESG risk exposure that smaller companies face: Revolving around how CSRD value chain requirements and lender ESG criteria apply regardless of size.

What Is Environmental, Social and Governance Risk?

ESG risk refers to the financial, operational, and reputational threats that arise from a company’s exposure to environmental, social and governance factors. It is not a single risk category. It is a lens through which a broad range of sustainability risks — from carbon exposure to board misconduct — can be identified, measured, and managed across the entire business model.

The distinction worth establishing early: ESG risk is not the same as ESG performance. A company can publish a polished sustainability report while carrying significant unmanaged exposure. Understanding ESG risks means looking beneath the disclosures at where the real risk sits: in the supply chain, in governance structures, in how the business is positioned relative to incoming regulation.

The financial case for taking it seriously is straightforward. Research consistently links strong ESG risk management to lower cost of capital, better access to institutional investment, and more resilient earnings over long periods.

The reverse is equally well-documented. Financial losses arising from ESG-related incidents — regulatory fines, operational disruption, reputational damage can be severe and fast-moving. For companies operating in European markets, where the regulatory environment for sustainability reporting is among the most developed globally, the cost of under-investment in ESG risk management is rising year on year.

Types of ESG Risk

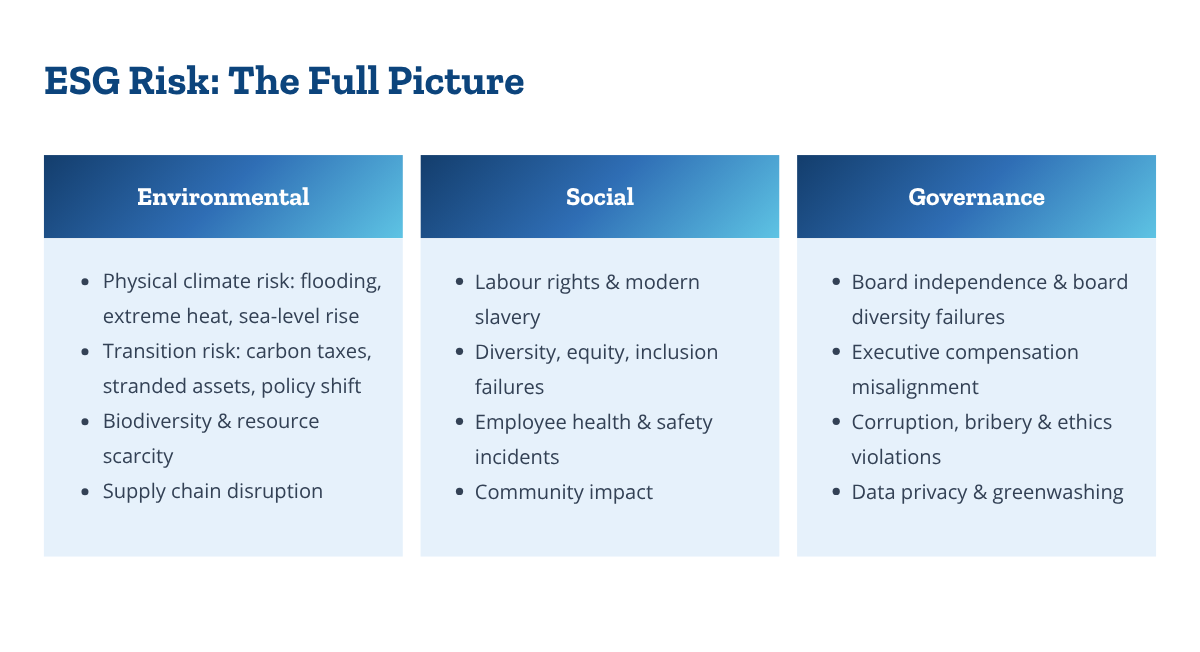

ESG risk does not arrive in a single form. It spans three distinct but interconnected pillars, each with its own drivers, timelines, and financial implications. The taxonomy matters, because different risk types require fundamentally different management approaches.

Environmental Risks

Environmental risks arise from a company’s relationship with the natural world: both how its operations affect the environment and how environmental change affects its operations. Resource depletion, pollution, biodiversity loss, and the increasing frequency of extreme weather events all fall within this category.

For most companies, the most material environmental exposure sits in the supply chain. Raw material dependency, water scarcity in manufacturing regions, and deforestation risk in agricultural supply chains are all environmental risks that can trigger operational disruption long before they trigger a formal disclosure obligation.

Your Scope 3 supply chain exposure is harder to quantify than it looks.

Climate Risk: Physical and Transition Exposure

Climate risk deserves its own treatment within the environmental category, because it operates on two distinct tracks that risk management functions frequently conflate.

Physical risks are the direct consequences of climate change: flooding, extreme heat, sea-level rise, and increasingly frequent climate related events that damage assets, disrupt logistics, and drive up energy costs and operational costs.

These are not theoretical future risks. According to the European Environment Agency and industry loss data from insurers including Munich Re, climate-related events in Europe in 2024 generated economic losses running to billions of euros, affecting Germany, Italy, France, Spain, and Central and Eastern Europe.

Transition risks arise from the shift to a low-carbon economy. Carbon taxes, policy tightening, shifting investor preferences, and the risk of stranded assets all sit here. Commercial real estate portfolios face growing transition risk as EU net-zero commitments drive demand for energy-efficient properties and push older, less efficient stock toward reduced valuations. Carbon emissions that go unmanaged today become transition liabilities tomorrow.

The TCFD framework (widely adopted voluntary recommendations, now embedded in several regulatory regimes) asks companies to assess both physical and transition risk through scenario analysis i.e. stress-testing the business model against multiple climate pathways.

The TNFD (Taskforce on Nature-related Financial Disclosures, a voluntary framework launched in 2023) extends this logic to nature-related risks, covering biodiversity loss and ecosystem dependency.

TNFD is not yet an EU regulatory requirement, but uptake among European companies is accelerating, with hundreds of organisations already reporting voluntarily under the framework globally.

Social Risks

Social risks cover how a company manages its relationships with people: Employees, local communities, customers, and the broader society in which it operates.

Labour rights violations, poor employee health and safety practices, modern slavery in supply chains, and failures on diversity and inclusion all represent social risks with direct financial consequences. Legal action, operational disruption, loss of consumer trust, and reputational damage are the typical transmission mechanisms.

The lesson from high-profile ESG examples — Nike’s supply chain labour scandals, the Rana Plaza disaster is consistent and tells us how the financial and reputational cost of inaction significantly exceeds what proactive management would have required.

Social risk is also evolving. As stakeholder expectations around corporate responsibility sharpen and as CSRD and the EU Corporate Sustainability Due Diligence Directive (CSDDD, politically agreed in 2023, formally adopted in 2024, with member states required to transpose it into national law by July 2026) place formal obligations on companies regarding their value chain impacts — social risks that were once considered reputational are acquiring legal dimensions.

Human rights due diligence is no longer optional for companies of meaningful scale operating in European markets.

Governance Risks

Governance risks arise when the structures meant to keep a company accountable fail ( or were never properly built).

Governance factors include board diversity and independence, executive compensation structures, anti-corruption and bribery controls, data privacy practices, and the quality of internal audit and oversight.

Weak governance practices create the conditions for other ESG risks to compound: A board that cannot meaningfully challenge management on climate exposure is a governance risk that amplifies a physical risk.

Greenwashing sits increasingly within the governance risk category, and it is worth treating it as such. The European supervisory authorities — ESMA, EBA, and EIOPA — have significantly increased their scrutiny of ESG-related claims, with ESMA taking a particularly active role in supervising ESG ratings providers and issuing guidance on greenwashing risk.

EBA supervisory reports have flagged growing greenwashing concerns across the European financial sector, and the direction of regulatory travel is clearly toward enforcement rather than guidance.

Misrepresenting ESG performance — whether to investors, lenders, or regulators — is no longer just a reputational problem. It is becoming a legal and financial one.

ESG Risk vs. Traditional Financial Risk

Risk managers who have spent careers working with financial risk models will recognise the structural logic of ESG risk management: identify, assess, mitigate, monitor. What makes ESG related risks materially different is not the process. It is the nature of the inputs.

Traditional financial risk operates on quantitative data with established measurement conventions and decades of precedent. ESG data is frequently incomplete, inconsistent across reporting entities, and difficult to verify — particularly when it originates from suppliers or value chain partners who are not themselves subject to mandatory disclosure requirements. The further into the supply chain you look, the thinner the data gets.

The time horizons are also different. Physical risks from climate change may not fully materialise for a decade or more but the capital allocation decisions being made today will determine whether a company is exposed when they do. Standard risk management processes are not designed for non-linear, long-horizon uncertainty of this kind.

Finally, ESG factors can be systemic rather than idiosyncratic. A carbon tax affects an entire sector simultaneously. A severe drought affects all companies dependent on water in a given region at the same time.

These risks do not diversify away within a portfolio. They require a category of management response that traditional risk frameworks were not built to accommodate and that is precisely why integrating ESG into Enterprise Risk Management, rather than running it as a parallel function, is the approach that works.

ESG Risk Assessment Methods and Frameworks

You do not need to build your ESG risk assessment framework from scratch. Several mature frameworks exist, and the regulatory landscape is increasingly prescriptive about which ones to apply.

TCFD (Task Force on Climate-related Financial Disclosures) is the foundational assessment method for climate risk disclosure, structured around four pillars: governance, strategy, risk management, and metrics and targets.

Where to find them? – https://www.fsb-tcfd.org/

Scenario analysis is TCFD’s defining contribution, requiring companies to model how their business model holds up under different climate pathways. For companies reporting under CSRD, ESRS E1 aligns closely with TCFD’s concepts, requiring similar disclosures across governance, strategy, risk management, and scenario-based metrics and targets.

TNFD (Taskforce on Nature-related Financial Disclosures) is a voluntary framework, launched in 2023, that applies equivalent logic to nature-related risks. Where TCFD asks about carbon and climate, TNFD asks about biodiversity dependency, ecosystem services, and nature-related transition risks.

For companies with operations or supply chains in nature-sensitive regions, TNFD is becoming an increasingly relevant assessment consideration, with hundreds of organisations (as of 2025) already reporting voluntarily under the framework globally.

Where to find them? – https://tnfd.global/

EBA ESG Risk Management Guidelines (2025) were finalised for financial institutions, but their framework logic — integrating ESG factors into risk appetite statements, credit assessment, and internal capital adequacy processes — is directionally relevant for any corporate risk function seeking to align with best practice.

The EBA’s approach of treating ESG as a driver of conventional risk categories (credit risk, market risk, operational risk) rather than as a standalone category is a useful model for corporate ERM integration.

Where to find them? – (EBA’s website is broken, here’s another link)

CSRD Double Materiality is arguably the most operationally significant development for companies reporting under European law. Double materiality requires assessing ESG risk from two directions simultaneously: how sustainability issues affect the company financially (financial materiality), and how the company’s activities affect people and the environment (impact materiality).

The double materiality assessment, aligned with the European Sustainability Reporting Standards, is effectively a structured risk identification exercise. Companies that complete it rigorously produce, as a by-product, the most comprehensive ESG risk register they have ever had.

Where to find them? – https://ec.europa.eu/newsroom/fisma/items/754701/en

The Global Reporting Initiative and the SASB Standards (now maintained under the IFRS Foundation as part of the ISSB’s work on industry-specific sustainability disclosure) provide the underlying frameworks that most risk assessment processes draw on.

GRI’s standards remain the most widely adopted globally for impact-focused reporting. The SASB industry-specific materiality maps are particularly useful for calibrating which ESG factors carry financial relevance within a given sector – an important efficiency gain when resources for ESG risk management are constrained.

Where to find them? – https://www.globalreporting.org/ | https://www.ifrs.org/

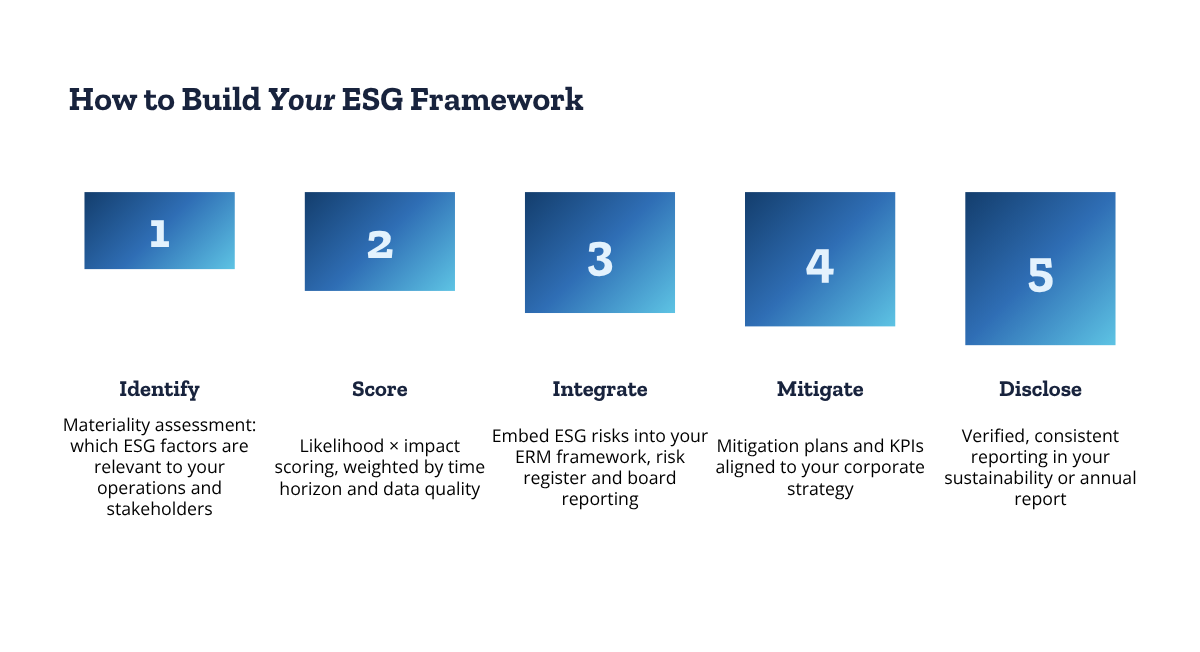

Risk Management Strategies: How to Build Your ESG Framework

An effective ESG risk management framework does not need to be built in isolation from everything else. The most durable approach integrates ESG factors into existing Enterprise Risk Management structures the same risk registers, risk appetite statements, and board reporting processes that govern financial and operational risk.

ESG that lives only in the sustainability report and never reaches the board or the CFO is not being managed. It is being disclosed.

Step 1: Risk Identification via Materiality Assessment

The starting point is a materiality assessment: identifying which ESG factors are relevant to your business activities, your sector, and your stakeholder base. CSRD’s double materiality methodology provides the most rigorous current approach.

The output is a prioritised list of potential risks and opportunities that becomes the foundation for everything that follows. Credibl’s platform maps materiality assessments directly to CSRD and ESRS regulatory requirements, so risk identification and reporting preparation happen within the same workflow rather than as separate exercises.

Step 2: Risk Scoring

Once risks are identified, they need to be scored — typically by likelihood and magnitude of impact, with a weighting for time horizon. ESG data quality is the critical variable at this stage. Quantitative inputs (carbon footprint, water consumption, energy consumption, workforce diversity metrics) provide the most reliable scoring foundation.

Where data is incomplete, scenario-based qualitative assessment fills the gap. The assessment method should be documented and auditable particularly for companies subject to CSRD’s limited assurance requirements, which are in force now and moving towards reasonable assurance by 2028.

Step 3: Integration into Enterprise Risk Management

ESG risks that score above materiality thresholds should sit inside the company’s main risk register alongside financial and operational risks. This is where decision making processes align with ESG exposure. Risk owners need to be assigned.

Board-level reporting needs to reflect material ESG risks in the same language as other principal risks. The ESG strategy should not be a separate document that runs parallel to the business strategy. It should be the same document.

Step 4: Mitigation Planning and KPI Setting

Each material ESG risk requires a mitigation response and a measurable set of KPIs.

- For environmental risks, this might mean carbon emissions reduction targets and supply chain engagement programmes.

- For social risks, it might mean supplier human rights audits and workforce health and safety metrics.

- For governance risks, it might mean board diversity reviews or anti-corruption training completion rates.

The KPIs should be integrated into corporate strategy and tracked at the same cadence as financial performance indicators. Treating them as annual reporting inputs rather than operational management tools is one of the most common failure modes in ESG risk management programmes.

Step 5: Disclosure in the Sustainability or Annual Report

Disclosure is the output of the framework, not the goal. A company that has genuinely integrated ESG risk management into its company’s operations will find the disclosure process considerably less painful, because the data exists, has been verified, and is consistent with what the financial statements say.

Non compliance with disclosure requirements is a regulatory risk in itself. But the deeper problem for companies that approach disclosure as a starting point rather than an endpoint is that the data is usually unreliable. Which makes it a governance risk too.

Managing Carbon Emissions Within Your Framework

Carbon emissions warrant specific attention within any ESG risk framework, both because of their financial materiality and because of the precision now demanded by regulators. Scope 1 and 2 emissions are relatively tractable.

Scope 3 — the indirect emissions across the value chain — is where the majority of most companies’ carbon footprint exposure sits, and where risk management programmes have historically been the weakest.

CSRD requires Scope 3 disclosure where material, with methodology alignment expected to follow the GHG Protocol. The EU’s Carbon Border Adjustment Mechanism (CBAM) is creating additional regulatory risks for companies with carbon-intensive supply chains touching the EU.

Transitional CBAM reporting obligations have been in force since October 2023; the full financial mechanism, including payment obligations, is currently planned for application from October 2026. For companies still treating Scope 3 as a future problem, the regulatory clock is already well into its countdown.

How to Mitigate ESG Risk with Technology

The manual approach to ESG risk management — spreadsheets, email chains, disconnected data sources — creates audit risk, introduces errors, and makes it nearly impossible to produce consistent, comparable ESG data across reporting periods. Many businesses are still running their ESG programmes this way. The problem is not discipline. It is infrastructure.

Purpose-built ESG software addresses the core data challenge: collection from multiple sources, version control on emission factors, automated mapping to frameworks (TCFD, CSRD, GRI, SASB), and audit-ready outputs.

The difference between an ESG risk programme that genuinely informs decision making and one that merely produces compliance documents is, in most cases, a data infrastructure problem. Getting the plumbing right is not a glamorous task. It is, however, the one that makes everything else work.

Third-party ESG investments in external ratings platforms — Sustainalytics, MSCI, S&P Global — provide useful benchmarking of ESG risk exposure relative to sector peers. These are valuable inputs for investor communication and for calibrating internal scores against market expectations.

Note: ESG rating methodologies differ significantly across providers, and ratings for the same company can diverge materially depending on the framework and data sources used. They are useful reference points, not definitive verdicts. External ratings assess how a company looks from the outside. Internal frameworks determine what is actually being managed.

Credibl maps ESG risks to your materiality assessment, CSRD disclosure requirements, and internal KPI tracking within a single platform — so your risk programme and your reporting programme are the same programme rather than two teams producing overlapping spreadsheets.

ESG Risk Considerations for Smaller Companies

A common assumption is that ESG risk management is the domain of listed multinationals with dedicated sustainability teams.

The regulatory perimeter is widening, and smaller companies are increasingly finding themselves inside it — through supply chain due diligence requirements placed on them by large customers, through CSRD’s extended reach into the value chains of in-scope companies, and through the EU’s new Voluntary Sustainability Reporting Standard (VSME), which provides a structured ESG framework specifically designed for SMEs.

The business case for smaller companies to manage ESG risks is straightforward and does not depend on regulatory compulsion alone.

Access to finance increasingly incorporates ESG data — banks and investors are applying ESG criteria to lending and investment decisions in ways that affect cost of capital directly. Consumer trust, talent acquisition, and supplier qualification processes all carry ESG exposure for companies of any size. And as large companies face their own CSRD obligations, they are pushing ESG data requirements down their supply chains to smaller suppliers who may not have seen it coming.

The good news is that smaller companies do not need enterprise-scale ESG programmes to manage their most material risks.

A focused materiality assessment, basic Scope 1 and 2 carbon emissions measurement, and governance documentation provide a credible foundation. Companies stay competitive not by doing everything, but by managing the risks that are actually material to their business model.

The VSME’s modular structure — a basic tier covering key sustainability indicators most requested by value chain partners and financial institutions, and a comprehensive tier for companies with more advanced stakeholder requirements — is designed precisely for this.

The sustainability journey does not need to begin at the finish line. It needs to begin where the risk is. For most smaller companies, that means energy consumption, supply chain exposure, and governance basics — not a thousand-data-point CSRD report.

Managing ESG Risk Is a Business Decision, Not a Reporting Exercise

ESG risk has moved from the corporate responsibility department to the boardroom, and from the boardroom to the finance function.

Regulatory frameworks are formalising what capital markets have been pricing for years: that unmanaged sustainability risks tend to become financial ones, usually at the worst possible moment.

The companies navigating this well are not those with the longest sustainability reports. They are those that have embedded ESG risk management into how they make decisions about capital allocation, supply chain partners, governance structures, and long term success. The frameworks are available. The data infrastructure is improving. The regulatory requirements are clear enough to act on.

What separates the companies that manage ESG risks well from those that encounter their exposure through a fine or a headline is, in most cases, simply the decision to start.

So, the cost of a conversation is considerably lower than the cost of finding out the hard way.

Let’s Talk.

FAQs

What Is ESG Risk?

ESG risk refers to the financial, operational, and reputational threats arising from a company’s exposure to environmental, social, and governance factors. It is not a standalone risk category but a lens for identifying material sustainability risks across the business model: from carbon exposure and supply chain disruption to board governance failures. Unlike ESG performance, which measures outcomes, ESG risk measures exposure.

What Are the Three Types of ESG Risk?

ESG risks fall into three categories. Environmental risks include physical climate risk (flooding, extreme heat), transition risk (carbon taxes, stranded assets), and biodiversity loss. Social risks cover labour rights violations, modern slavery, health and safety failures, and community impact. Governance risks include board independence failures, executive compensation misalignment, corruption, and greenwashing.

How Does ESG Risk Differ from Traditional Financial Risk?

ESG risk differs in three key ways: it operates over longer time horizons, relies on harder-to-quantify data, and can be systemic, affecting entire industries simultaneously rather than individual companies. A carbon tax or severe drought does not diversify away within a portfolio. Standard risk management processes are not designed for this kind of non-linear, long-horizon exposure.

How Do You Assess ESG Risk?

A structured ESG risk assessment follows five steps: identify material risks via a materiality assessment, score them by likelihood and impact, integrate them into your existing enterprise risk management framework, build mitigation plans with measurable KPIs, and disclose findings in your sustainability or annual report. CSRD’s double materiality methodology is currently the most rigorous assessment method available for European companies.

Do Smaller Companies Need to Manage ESG Risk?

Yes. Smaller companies face ESG risk exposure through three routes: supply chain due diligence requirements from large customers operating under CSRD, lender and investor ESG criteria that directly affect cost of capital, and the VSME (Voluntary Sustainability Reporting Standard for non-listed Small and Medium-sized Entities), adopted by the European Commission in July 2025 and designed specifically for companies at this stage.