On February 26, 2025, the European Commission unveiled the Omnibus Directive, a legislative proposal designed to overhaul the EU’s sustainability and corporate reporting landscape significantly. Officially termed the “Omnibus Simplification Package,” this initiative aims to amend key directives such as the Corporate Sustainability Reporting Directive (CSRD) and the Corporate Sustainability Due Diligence Directive (CSDDD) and strike a delicate balance between the ambitious sustainability goals of the European Green Deal and the pressing need to reduce regulatory burdens on businesses.

At its core, this directive responds to growing concerns from businesses and policymakers alike, advocating for a streamlined yet effective regulatory framework that bolsters competitiveness without compromising environmental and social objectives. It still raises important questions about the future trajectory of the EU’s ambitious sustainability agenda.

Background: The Need for Simplification

The CSRD and CSDDD have been instrumental in enhancing transparency and accountability in corporate sustainability practices. However, as these directives rolled out, businesses, particularly Small and Medium Enterprises (SMEs), began to feel the weight of compliance costs and administrative burdens. The economic pressures exacerbated by Russia’s war against Ukraine, soaring energy prices, and a shifting geopolitical landscape further intensified calls for regulatory relief.

EU leaders, through initiatives such as the Budapest Declaration on the New European Competitiveness Deal, urged a “simplification revolution” to drastically reduce administrative, regulatory, and reporting burdens by 25% by mid-2025. The European Commission’s Communication on the Competitive Compass for the EU solidified this intent, promising a Simplification Omnibus package with far-reaching measures to ease compliance in sustainable finance reporting, sustainability due diligence, and taxonomy requirements.

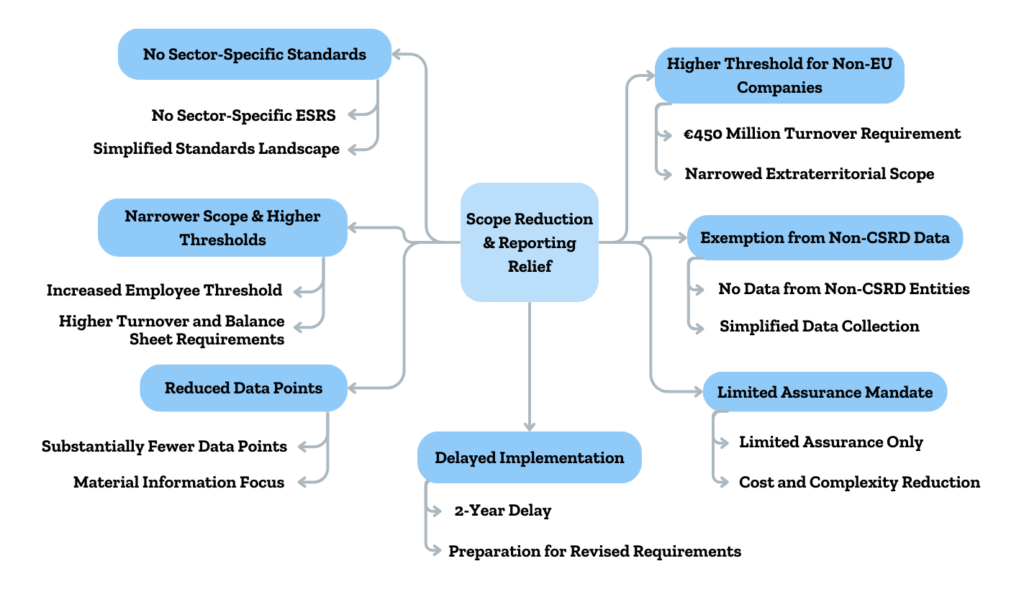

The Changes and Simplifications: Scope Reduction and Reporting Relief

The proposed amendments to the CSRD represent a notable shift in its scope and reporting requirements:

- Narrower Scope & Higher Reporting Thresholds: The most impactful change is the significant reduction in the number of companies subject to CSRD. The employee threshold has been dramatically increased from 250 to over 1000 employees. Additionally, companies now need to exceed either €50 million in turnover or €25 million on their balance sheet to fall under the CSRD’s purview. This drastically reduces the number of companies obligated to report.

- Exemption from Non-CSRD Data: Companies will be relieved from the obligation to obtain sustainability data from entities outside the CSRD scope. This addresses a major pain point for businesses struggling to collect data from their entire value chain, particularly from smaller suppliers.

- Limited Assurance Mandate: The package mandates only limited assurance for sustainability reporting, removing the previously anticipated transition to reasonable assurance. This lowers the immediate cost and complexity associated with audits and verification.

- Substantially Reduced Data Points: The European Sustainability Reporting Standards (ESRS), the detailed rules for CSRD reporting, will be revised to reduce the number of mandatory data points dramatically. This aims to focus on reporting on the most material information, simplifying the process and potentially making reports more relevant.

- No Sector-Specific Standards: The proposal removes the power to adopt sector-specific ESRS standards. This simplifies the standard landscape, although it may reduce the granularity and relevance of reporting for specific industries.

- Higher Reporting Threshold for Non-EU Companies: The threshold for non-EU parent companies to report has been raised significantly from €150 million to €450 million in EU turnover, further narrowing the scope of extraterritorial application.

- Delayed Implementation: A ‘stop the clock’ proposal suggests a 2-year delay for large undertakings and listed SMEs not yet implementing CSRD. This provides additional breathing room for companies to prepare for the revised requirements.

Key aspects of the EU sustainability reporting and due diligence framework before and after the Omnibus proposal:

| Aspect | Before Omnibus | After Omnibus |

| Scope of Sustainability Reporting (CSRD) | – Mandatory reporting applied to large undertakings, listed SMEs, and other specified groups based on previous thresholds. | – Mandatory reporting limited to large undertakings with more than 1,000 employees only. Listed SMEs and some large undertakings are removed from the mandatory scope. |

| Scope of Corporate Sustainability Due Diligence (CSDDD) | – Due diligence obligations applied more broadly across value chains, including indirect business partners. | – Obligations are now more focused on direct business partners. Indirect partners are only assessed if there is credible information suggesting potential or actual adverse impacts. |

| Reporting Standards (ESRS) | – ESRS included both sector-agnostic and sector-specific standards, with numerous mandatory datapoints. | – Revision of ESRS reduces mandatory datapoints (focusing on quantitative data), removes sector-specific standards, and differentiates between mandatory and voluntary disclosures. |

| Monitoring Frequency (Due Diligence) | – Companies were expected to conduct annual monitoring exercises. | – Monitoring intervals are extended from one year to five years, with ad hoc assessments possible if needed, reducing administrative burden. |

| Stakeholder Engagement in Due Diligence | – Engagement with a broad range of stakeholders was required at several stages of the due diligence process. | – The scope is narrowed to require engagement only with “relevant” stakeholders directly linked to the specific stage of the due diligence process. |

| Alignment and Harmonisation | – Some discrepancies existed between sustainability reporting (CSRD) and due diligence (CSDDD) frameworks, with overlapping obligations. | – Adjustments align thresholds and definitions between CSRD and CSDDD, ensuring that companies subject to both are not required to report duplicate information, thereby streamlining compliance. |

| Value-Chain Reporting | – Reporting requirements on the value chain could extend to smaller suppliers, sometimes imposing burdens on SMEs. | – Introduction of a strengthened “value-chain cap” limits reporting obligations from affecting SMEs (those with up to 1,000 employees) by protecting them from excessive information requests. |

Positive Impacts and Opportunities: Efficiency and Competitiveness

The Omnibus Package is projected to bring several positive impacts and opportunities:

- Reduced Regulatory Burden: The most immediate and significant impact is the anticipated reduction in regulatory burden for businesses across the EU. The narrowed scope of CSRD, exemptions for SMEs under the Taxonomy, and streamlined reporting requirements are all designed to ease compliance.

- Cost and Administrative Savings: Simplified processes and reduced reporting requirements translate directly into cost and administrative savings for businesses. This can free up resources for investment, innovation, and core business activities.

- More Effective Reporting: By focusing on material data points and streamlining reporting standards, the package aims to make sustainability reporting more focused, efficient, and ultimately more useful. This could lead to better quality information for investors and stakeholders.

- Increased Competitiveness: By easing regulatory burdens, the Omnibus Package seeks to boost economic competitiveness within the EU, ensuring that sustainability ambitions do not come at the expense of business viability.

- Investment in Clean Energy: The package is presented alongside the Clean Industrial Deal and InvestEU amendments, which aim to boost clean energy adoption and investment. The simplification measures are intended to complement these broader initiatives, making the green transition more economically feasible.

What Remains Unchanged: Core Principles Maintained

Despite the significant simplifications, certain core principles of the EU’s sustainability framework remain untouched:

- Double Materiality Principle: The fundamental double materiality principle of CSRD reporting, which requires companies to report on both their impact on people and the planet (impact materiality) and how sustainability issues affect their financial performance (financial materiality), is maintained.

- Assurance Requirements: While the level of assurance is set at limited assurance, the requirement for independent assurance of sustainability information remains in place, ensuring a degree of credibility and reliability in reported data. Companies must still adhere to the same assurance requirements as originally intended for CSRD reporting (albeit at a limited assurance level).

A Step Toward Smarter Regulation

The Omnibus proposal is now entering the EU’s legislative process, which involves scrutiny and agreement from both the European Parliament and the EU Council. This process can involve further amendments and negotiations before the package is finalized. If approved, the Omnibus Package will become a Directive, requiring each EU member state to incorporate its provisions into national law.

The Omnibus Directive represents a significant step forward in creating a simpler, smarter regulatory framework for corporate sustainability and due diligence. By reducing compliance costs, introducing voluntary standards, and enhancing regulatory proportionality, the proposal has the potential to boost EU competitiveness while supporting the green transition. However, its success will depend on effective implementation and the willingness of companies to embrace voluntary reporting as a strategic advantage rather than a regulatory burden.

Join the conversation and share your thoughts on how these regulatory changes might reshape corporate sustainability in Europe. We’d love to hear your perspective—what challenges and opportunities do you see emerging from the Omnibus Directive? Leave your comments below or follow our LinkedIn Page for more insights and updates on the evolving sustainability landscape.