The Asia-Pacific (APAC) region is rapidly emerging as a leader in sustainability reporting transformation, driven by a growing alignment with the International Sustainability Standards Board (ISSB) framework. Since the launch of IFRS S1 and S2 in mid-2023, several economies including Japan, Indonesia, Singapore, and India have initiated or accelerated efforts to adapt and localise these global standards. As of early 2025, 28 jurisdictions representing 57% of global GDP have shown commitment to ISSB-aligned disclosures.

Japan is leading the charge in APAC with the official release of its Sustainability Disclosure Standards through the Sustainability Standards Board of Japan (SSBJ) on March 5, 2025. Meanwhile, countries like Indonesia are in advanced consultation phases, and Singapore has announced plans to mandate climate-related disclosures in alignment with IFRS S2 by 2027 for listed companies and large non-listed companies.

This rising momentum reflects a regional acknowledgement that ISSB compliance is no longer just a global best practice — it’s becoming a business imperative. As capital markets increasingly factor sustainability into valuation, APAC economies are aligning disclosure norms to remain competitive and attract global investment.

Localization in Practice: Japan’s Three-Part Adaptation

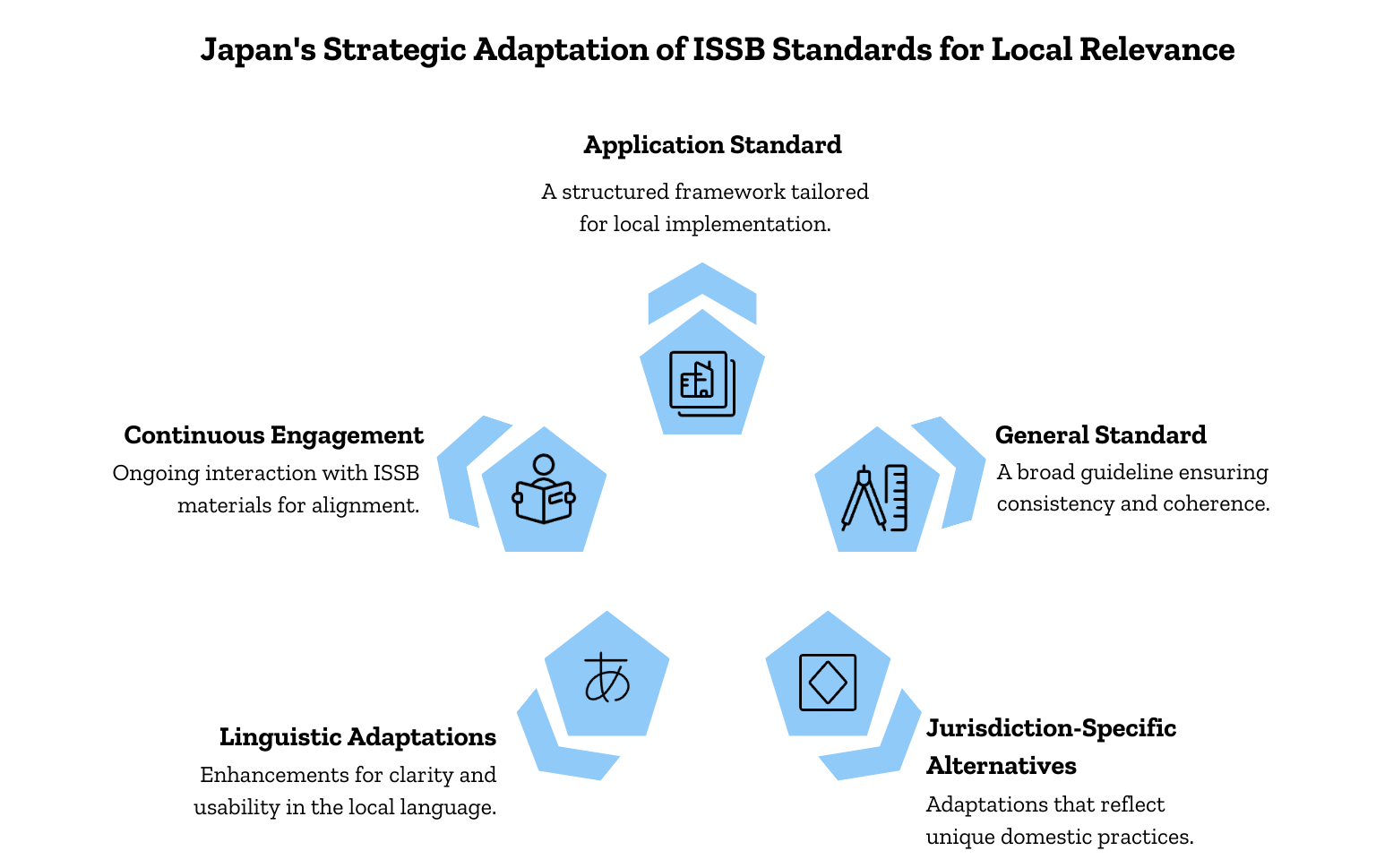

Japan’s approach to ISSB localization illustrates how jurisdictions are tailoring standards without diluting their integrity. Instead of directly applying IFRS S1 and S2, the SSBJ divided IFRS S1 into two distinct parts — the Application Standard and the General Standard — bringing the total to three standards. All three, however, are meant to be applied together to preserve coherence with the ISSB framework.

Beyond structural tweaks, Japan also introduced optional, jurisdiction-specific alternatives, especially to cater to domestic business practices and legal contexts. Linguistic adaptations were made to enhance the flow and clarity of content in Japanese, ensuring usability for local stakeholders.

These nuanced changes exemplify a balancing act between international comparability and local relevance. Notably, the SSBJ has committed to continuous engagement with ISSB educational materials and updates, ensuring alignment stays current.

Other countries are taking similar paths:

- Singapore’s Accounting and Corporate Regulatory Authority (ACRA) and SGX are expected to release their roadmap for ISSB-compliant disclosures in Q2 2025.

- India’s SEBI (Securities and Exchange Board of India) is also exploring ISSB-aligned reporting under its Business Responsibility and Sustainability Reporting (BRSR) Core framework.

Voluntary Today, Mandatory Tomorrow? The Strategic Shift

While the current standards in Japan remain voluntary, there’s a strategic undertone suggesting that mandatory adoption is imminent, particularly for companies listed on the Tokyo Stock Exchange Prime Market. This mirrors a growing global trend where voluntary reporting serves as a preparatory phase for future compliance.

According to the 2024 Verdantix Global Corporate ESG Survey, over 50% of firms ranked voluntary ESG reporting standards as a top-three priority, indicating a strong proactive stance from the private sector. Moreover, interoperability between voluntary and mandatory frameworks is becoming essential, especially as overlapping data needs emerge across jurisdictions.

The ISSB’s alignment with the TCFD (Task Force on Climate-related Financial Disclosures) and its influence on the EU’s CSRD (Corporate Sustainability Reporting Directive) further amplifies this. In effect, firms engaging in voluntary ISSB-aligned disclosures are also preparing for compliance in Europe, the UK, and other regions — mitigating regulatory risk and improving investor transparency in one move.

Investor Demands, Market Signalling & Strategic Risk

Investor influence is one of the most powerful catalysts behind the surge in voluntary ESG reporting. Global asset managers, including BlackRock, State Street, and Norges Bank Investment Management, have consistently emphasized the need for standardized, decision-useful ESG data.

A recent analysis by Morningstar revealed that sustainable fund assets in APAC reached $57 billion in 2024, with Japan accounting for over 35% of these inflows. This underscores a key market signal: firms not disclosing climate-related risks and opportunities risk losing investor favour.

By voluntarily adopting ISSB standards, companies are not only enhancing transparency but also positioning themselves strategically in capital markets. This is particularly relevant in sectors like manufacturing, energy, and finance, where climate-related risks can materially impact valuations and investor confidence.

Japan’s move, and the signals coming from countries like Indonesia and Singapore, highlight how investor demand is shaping the regulatory narrative—pushing regulators to close the gap between voluntary reporting and enforceable mandates.

Case in Focus: Indonesia, Singapore & India – Who’s Next?

As Japan sets the tone, other APAC nations are following closely behind, each bringing their flavour to the ESG disclosure landscape.

Indonesia

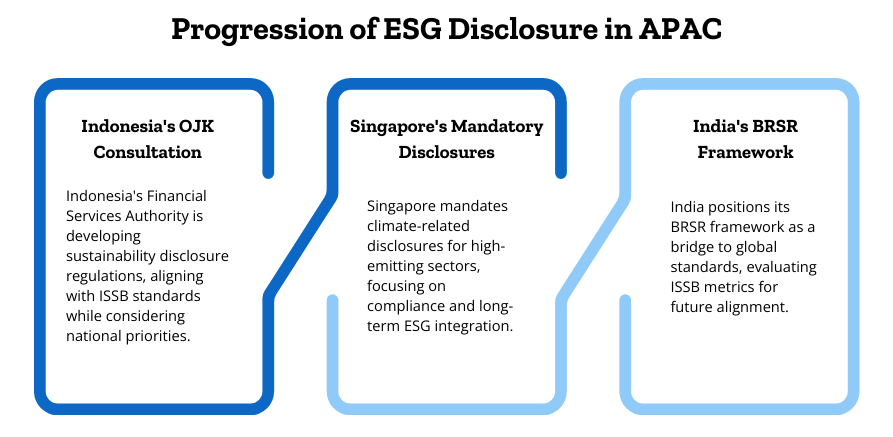

Indonesia’s Financial Services Authority (OJK) is actively developing sustainability disclosure regulations that incorporate ISSB standards. In late 2024, the OJK launched a public consultation on draft climate-related disclosure rules aimed at listed companies and large financial institutions. The proposed framework mirrors IFRS S2, requiring entities to disclose governance, strategy, risk management, and metrics & targets related to climate risks. Indonesia’s approach is strategic—balancing international alignment with national developmental priorities, especially given its fossil-fuel-reliant economy and vulnerability to climate impacts.

Singapore

Singapore, often seen as the ESG hub of Southeast Asia, continues to lead with regulatory clarity. In October 2023, the Accounting and Corporate Regulatory Authority (ACRA) and Singapore Exchange (SGX) announced that climate-related disclosures aligned with ISSB’s IFRS S2 will become mandatory from FY2025 for listed issuers in high-emitting sectors, and from FY2027 for all large non-listed companies. Singapore’s focus is not just on compliance, but also on enabling businesses to integrate ESG into long-term strategy—backed by government grants, educational resources, and digital platforms.

India

India is charting its path through its Business Responsibility and Sustainability Reporting (BRSR) Core framework, made mandatory for the top 1,000 listed companies by SEBI. While not directly ISSB-aligned, BRSR shares key disclosure pillars and is being positioned as a bridge framework that could evolve in sync with global standards. In late 2024, SEBI formed a technical committee to evaluate how ISSB-aligned metrics can be incorporated into future iterations of BRSR, especially as Indian companies seek deeper access to international capital markets.

These countries represent a microcosm of the global ESG transition, showing how economies are moving in lockstep with ISSB while tailoring frameworks to national contexts. The convergence is clear—even with diverse paths, the destination is a more transparent, comparable, and accountable corporate world.

Conclusion: Voluntary Reporting as a Competitive Edge

The evolution of sustainability disclosures in APAC signals a paradigm shift from regulatory compliance to strategic alignment. As countries localize ISSB standards—while preserving their core principles—they are empowering businesses to meet not just policy expectations, but also investor demands and market pressures.

Voluntary ESG disclosure, once seen as optional, is now a strategic differentiator. Firms that adopt ISSB-aligned practices are positioning themselves for smoother transitions to mandatory regimes, improved access to capital, and enhanced stakeholder trust.

Japan’s formalisation of voluntary standards, Indonesia’s fast-track consultation, Singapore’s clear roadmap, and India’s structured experimentation form a regional blueprint that other economies may soon follow. As global momentum continues, businesses that delay alignment risk falling behind—both in compliance readiness and market credibility.

How Credibl Can Help Companies Navigate Emerging Standards?

As sustainability disclosure standards become more complex and fast-moving, platforms like Credibl are becoming essential partners in the sustainability journey. Credibl enables organizations to align with global frameworks such as ISSB, TCFD, GRI, and CSRD, providing tools that simplify reporting, ensure data accuracy, and support multi-jurisdictional compliance.

Whether you’re a listed firm in Japan adapting to SSBJ standards, or a growing enterprise in Singapore preparing for IFRS S2 compliance, Credibl helps bridge the gap between voluntary action and regulatory readiness. With robust analytics, real-time updates on standards, and tailored disclosure templates, Credibl empowers companies to stay ahead of sustainability reporting expectations and build lasting stakeholder trust.