Last updated: May 12, 2026

Calm waters can be misleading.

At first glance, US climate disclosure laws look quieter than they did a year ago. The federal government stepped back from mandatory climate reporting in early 2025, and for a moment, it felt like the pressure had lifted.

But the regulatory current didn’t disappear. It just moved.

Instead of one federal rule setting the pace, climate disclosure in the US is now being shaped state by state. California is already moving ahead with mandatory emissions reporting (first deadline: August 10, 2026), while New York, New Jersey, Illinois, and Colorado have introduced or advanced their own climate disclosure frameworks.

For large companies operating across multiple US markets, this is a more complex compliance reality than a single federal rule ever was. One regulator with one deadline is manageable. Five states, five timelines, and five different definitions of “doing business here” is a different kind of problem.

The question is no longer only, “What are the SEC climate disclosure rules?” It is also, “Which state applies to us, what does it require, and how soon do we need to be ready?” For companies taking climate change seriously, the answer now starts at the state level.

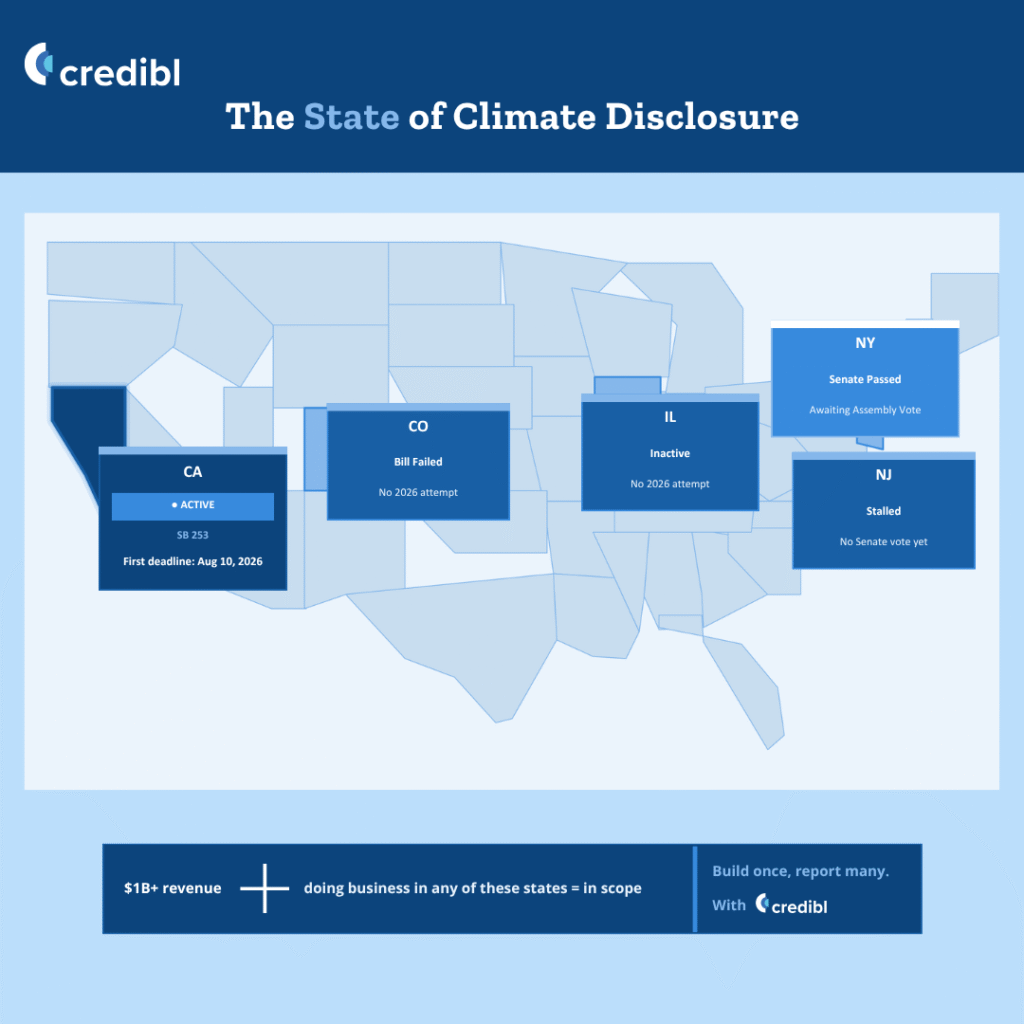

If your company clears $1 billion in annual revenue and operates in any major US market, at least one of these laws either already applies to you or likely will.

This tracker breaks down where each state stands, what’s required, and what multi-state companies should be doing right now.

Subscribe For Updates

Climate disclosure moves fast. Our tracker keeps up.

Drop your email below and we’ll send you updates the moment something changes.

Which US States Have Climate Disclosure Laws In 2026?

Five states have introduced or advanced climate disclosure legislation. One is fully active. One has passed its Senate and is awaiting Assembly action. Three are at earlier legislative stages.

Here’s the full picture at a glance:

| State | Bill | Status | Revenue threshold | Scope coverage | First reporting date | Penalty |

| California | SB 253 | Active (Law in effect) | >$1B | Scope 1 & 2 (2026), Scope 3 (2027) | August 10, 2026 | Up to $500,000/year |

| New York | S9072A | Passed Senate, awaiting Assembly | >$1B | Scope 1 & 2 (2028), Scope 3 (2029) | 2028 if enacted | Up to $500,000/year |

| New Jersey | S4117 | Stalled in Senate Budget committee | >$1B | Scope 1, 2 & 3 (phased) | TBD if enacted | Up to $50,000/offense |

| Illinois | HB 3673 | Referred to Rules Committee, not reintroduced | >$1B | Scope 1 & 2 (2027), Scope 3 (2027) | 2027 if enacted | TBD |

| Colorado | HB 25-1119 | Failed committee vote, not reintroduced | >$1B | Scope 1 & 2 (2028), Scope 3 (2029) | 2028 if enacted | TBD |

What Are State Climate Disclosure Laws And Why They Matter Now?

State climate disclosure laws require large companies doing business within a state to publicly report their greenhouse gas emissions — Scope 1, 2, and eventually Scope 3 — on an annual basis, verified by independent third parties.

The structure is largely consistent across states: revenue thresholds (typically $1 billion), GHG Protocol-aligned calculations, phased assurance requirements, and public registries managed by state agencies. Think of it as financial reporting logic applied to emissions data — same discipline, same consequences for getting it wrong. These frameworks capture both physical and transition risks — from flooding and supply chain disruption to stranded assets and regulatory cost exposure.

What makes these laws nationally significant is a detail buried in their scope definitions. Compliance is triggered by where you do business, not where you’re headquartered. These laws apply equally to public and private companies, the $1 billion threshold is based on total annual revenues, not listing status.

A retailer based in Texas, a manufacturer headquartered in Ohio, a financial services firm incorporated in Delaware — if you generate revenue from California or New York, you are in scope regardless of where your registered office sits. That’s the part many legal and compliance teams are still catching up with.

The federal retreat hasn’t slowed state momentum. If anything, it has accelerated it. With the SEC’s climate rule effectively shelved, states are filling the gap and they’re doing it with frameworks that closely mirror each other, which, as we’ll cover below, is actually useful news for companies trying to build one compliance infrastructure that works across jurisdictions.

California: The Law That’s Already In Effect

California moved first, and it moved decisively. SB 253 — the Climate Corporate Data Accountability Act — was signed into law in October 2023. The California Air Resources Board finalized implementing regulations in February 2026. The first deadline is August 10, 2026.

Here’s what the law requires: Business entities with more than $1 billion in total annual revenues doing business in California must publicly disclose their Scope 1 and Scope 2 greenhouse gas emissions — covering both direct emissions from owned or controlled sources and indirect emissions from purchased energy.

Scope 3 emissions — the harder part, covering your full value chain — follows in 2027. Emissions must be calculated using the GHG Protocol Corporate Accounting and Reporting Standard. Penalties for non-compliance run up to $500,000 per year.

One thing worth understanding clearly: CARB has indicated it will apply enforcement discretion for first-year filers acting in good faith. That is not an invitation to skip the deadline.

CARB’s own guidance states it expects all in-scope companies to report by August 10, and discretion is exercised on a case-by-case basis for companies that can demonstrate genuine compliance efforts. Companies that haven’t started are in a different category entirely.

A note on SB 261, California’s companion climate risk law: Enforcement is currently stayed by a Ninth Circuit injunction, following a legal challenge by the US Chamber of Commerce.

The stay applies only to SB 261. SB 253 is unaffected. The court could rule at any time, so companies that stopped preparing for climate risk disclosures are taking a calculated risk, but the August 10 emissions deadline is not in question.

For the full breakdown of both California laws, reporting timelines, and compliance requirements, see our California climate disclosure guide →

New York: The NY Climate Corporate Data Accountability Act (CCDAA)

New York is next in line. On February 10, 2026, the New York State Senate passed S9072A — the Climate Corporate Data Accountability Act — by a 40-22 vote along party lines. The bill now sits with the Assembly Codes Committee, where a companion bill, A4282, has also been introduced.

If enacted, S9072A would require companies with more than $1 billion in annual revenue doing business in New York to annually disclose their Scope 1, 2, and 3 greenhouse gas emissions.

Scope 1 and 2 reporting begins in 2028; Scope 3 follows in 2029. The New York Department of Environmental Conservation would oversee implementation and manage a public digital platform where all company disclosures would be accessible to investors, consumers, and regulators.

The enforcement mechanism is notably different from California’s. Rather than CARB, the New York Attorney General holds primary enforcement authority, with the power to bring civil actions against companies that fail to file, submit incomplete data, or — importantly — provide misleading information. Penalties run up to $100,000 per day, capped at $500,000 per reporting year.

For companies already building toward California SB 253 compliance, New York requires almost no additional architectural work. The frameworks are nearly identical — same GHG Protocol alignment, same phased assurance structure, same revenue threshold.

The main differences are a slightly later start date and modified Scope 3 safe harbor provisions that may offer more flexibility if your value chain data is still maturing. Building for California now effectively builds for New York simultaneously.

The bill still requires Assembly passage and the Governor’s signature before becoming law. Given the party-line Senate vote and the current political composition of the Assembly, passage is considered likely but not certain.

New Jersey: S4117 And What It Would Require

New Jersey introduced S4117 — its own Climate Corporate Data Accountability Act — in February 2025. The bill was referred to the Senate Budget and Appropriations Committee in March 2025 and has not advanced since. As of May 2026, it remains stalled in committee.

If enacted, S4117 would require companies with more than $1 billion in revenue doing business in New Jersey to disclose their Scope 1, 2, and 3 greenhouse gas emissions annually.

One practical detail worth noting: The bill explicitly allows companies to submit reports prepared for California’s SB 253 to satisfy New Jersey’s requirements. If you’re already filing in California, you’re most of the way there for New Jersey too.

Penalties under the proposed bill are lower than California’s:

- Up to $10,000 for a first offense

- $20,000 for a second, and

- $50,000 for subsequent violations

The New Jersey Department of Environmental Protection would administer the program, with a contracted nonprofit managing the public disclosure registry.

The bill’s current status reflects the broader legislative challenge of moving climate disclosure frameworks through committees in a politically divided environment.

That said, New Jersey has been directionally consistent on climate policy, and the bill’s alignment with California’s framework makes eventual passage more, not less, likely when the political window opens.

Illinois: HB 3673 And The Midwest’s Climate Disclosure Moment

Illinois introduced HB 3673 — the Climate Corporate Accountability Act — in February 2025, referring it to the House Rules Committee. The bill did not advance before the legislature adjourned and has not been reintroduced in the 2026 session as of the date of this publication.

If HB 3673 were enacted in its introduced form, it would require companies with more than $1 billion in revenue doing business in Illinois to disclose Scope 1 and 2 emissions beginning January 1, 2027, with Scope 3 following 180 days later.

The Secretary of State would have been required to finalize implementing rules by July 1, 2026.

Illinois is worth watching for two reasons.

First, it represents Midwest market exposure i.e. large manufacturers, agricultural supply chains, and financial services firms with Chicago operations would all be drawn into scope.

Second, the bill’s structure closely mirrors California’s, which means companies building GHG Protocol-aligned infrastructure today are already positioning themselves for Illinois compliance if and when the bill advances.

Colorado: Watching California’s Playbook

Colorado’s climate disclosure bill — HB 25-1119 — was introduced in early 2025 and proposed requiring companies with more than $1 billion in revenue doing business in the state to disclose Scope 1 and 2 emissions beginning in 2028 and Scope 3 by 2029. The bill lost an 8-5 vote in the House Committee on Energy and Environment and has not been reintroduced.

Colorado remains the least advanced of the five states covered here. It is included in this tracker because its legislative activity reflects the broader state-level disclosure movement, and because the Colorado market — energy, agriculture, technology — draws companies that are simultaneously in scope for California and potentially New York.

The direction of travel is clear even if the timing is not.

What Multi-state Companies Should Do Right Now?

One of these laws is active and has a deadline ~3 months away. One has passed a state senate. Three are at various stages of introduced, stalled, or inactive.

And yet the practical advice for a company above $1 billion in revenue doing business across multiple US states is the same regardless of which states are furthest along.

Here’s what that advice looks like in practice:

Build to GHG Protocol from day one

Every active and proposed state climate disclosure law requires emissions to be calculated using the GHG Protocol Corporate Accounting and Reporting Standard. Legislators rarely agree on anything. But they all agreed on this.

That alignment is your compliance strategy. Companies that invest in GHG Protocol-aligned data collection now are not just preparing for California.

They’re preparing for New York, and for whatever comes next in New Jersey and Illinois — without rebuilding their methodology from scratch each time a new state crosses the finish line.

Start Scope 3 readiness now, even if your immediate deadline is Scope 1 and 2

California’s Scope 3 deadline is 2027. New York’s is 2029 if the bill passes. But Scope 3 data — supply chain emissions, purchased goods, downstream product use — takes 12 to 18 months to build properly from scratch.

Companies that treat the Scope 1 and 2 deadline as the finish line will find themselves sprinting on Scope 3 with no runway.

Design your reporting infrastructure to satisfy multiple jurisdictions from one data layer

The states have made this easier than it looks: California compliance reports can be submitted directly to satisfy New Jersey’s requirements under S4117.

New York’s framework is close enough to California’s that a single reporting architecture covers both.

The goal is one structured, auditable dataset that produces outputs for whichever jurisdiction asks.

Fragmented tools and disconnected workflows make this harder and more expensive than it needs to be. The companies filing with confidence in August aren’t working across five spreadsheets — they’re using a unified system that ingests emissions data from invoices, utility bills, and supplier inputs, validates it, and produces audit-ready outputs across frameworks.

Have the assurance provider conversation now

California requires independent third-party assurance of emissions data, with limited assurance in early years and a transition to reasonable assurance over time.

New York’s bill anticipates third-party assurance, but the precise phasing and standards will depend on final implementing regulations if it is enacted.

Reasonable assurance is the same standard used for financial audits. Assurance provider capacity is finite, and the pipeline of companies needing these services is growing fast.

Companies that begin the conversation in 2026 will have options. Companies that wait until their first deadline is 60 days away will find those options considerably narrower.

The bottom line is that multi-state climate disclosure is a data and systems problem before it’s a reporting problem.

Companies that treat it as a reporting exercise — producing a document once a year — will rebuild their compliance infrastructure from scratch every time a new state law passes.

Companies that treat it as a data capability — structured, traceable, continuously maintained — shall only build once and report many times. With ease.

See how Credibl handles multi-jurisdictional reporting for you.

Frequently Asked Questions

Does my company need to comply with state climate disclosure laws if we’re not headquartered in California or New York?

Yes — and this is the detail most compliance teams miss. These laws are triggered by where you do business, not where you’re incorporated. If your company generates revenue from California and has more than $1 billion in annual revenue, SB 253 applies to you regardless of whether your headquarters is in Texas, Ohio, or anywhere else in the US.

What is the first deadline under US state climate disclosure laws?

California’s SB 253 sets the earliest deadline — August 10, 2026, for Scope 1 and 2 emissions reporting. This applies to all companies above $1 billion in annual revenue doing business in California. No other state climate disclosure law has an active deadline at this time.

Can we use our CSRD or TCFD report to satisfy SB 253?

Partially. CARB has confirmed that companies may submit existing sustainability reports that include Scope 1 and 2 emissions data calculated using the GHG Protocol. However, the report must be submitted directly to CARB’s reporting portal — simply publishing it on your website does not satisfy the requirement. If your CSRD report uses GHG Protocol methodology, it gives you a strong head start.

What is the NY Climate Corporate Data Accountability Act (CCDAA) and how does it differ from California’s SB 253?

The NY CCDAA — Senate Bill S9072A — passed the New York State Senate in February 2026 and mirrors California’s SB 253 closely. The key differences are a later start date (Scope 1 and 2 reporting begins in 2028 vs California’s 2026), modified Scope 3 safe harbor provisions, and enforcement by the New York Attorney General rather than CARB. Companies already building toward SB 253 compliance will need minimal additional work to satisfy New York.

What happens if we miss the SB 253 deadline?

CARB has stated it will apply enforcement discretion for first-year filers demonstrating good faith compliance efforts. However, the maximum civil administrative penalty for non-compliance is $500,000 per year — and “good faith” has a specific meaning. Companies that had not begun collecting GHG emissions data as of CARB’s December 2024 enforcement notice may submit a statement to that effect. Companies that simply missed the deadline without prior engagement with CARB are in a different position entirely.

Update Log

This log is updated every six weeks as per bill changes.

May 7, 2026 — Tracker published. California SB 253 August 10 deadline confirmed active. New York S9072A passed Senate February 10, 2026 — currently awaiting Assembly Codes Committee action. New Jersey S4117 remains stalled in Senate Budget and Appropriations Committee. Illinois HB 3673 not reintroduced in 2026 session. Colorado HB 25-1119 postponed indefinitely by House committee in February 2025, not reintroduced.

March 23, 2026 — CARB held public workshop reiterating August 10, 2026 as the firm SB 253 first reporting deadline. No extensions issued. CARB confirmed enforcement discretion applies only to companies demonstrating good faith compliance efforts.

February 26, 2026 — CARB adopted final SB 253 implementing regulations at its February board meeting, including key definitions for “doing business in California” and revenue thresholds.

February 10, 2026 — New York State Senate passed S9072A — the Climate Corporate Data Accountability Act — by a 40-22 party-line vote. Bill referred to Assembly Codes Committee. Companion bill A4282 introduced in the Assembly.

November 18, 2025 — US Court of Appeals for the Ninth Circuit granted injunction staying enforcement of SB 261. SB 253 emissions reporting requirements unaffected. CARB confirmed it will not enforce SB 261 pending appeal resolution.